The Iran War & Your Portfolio

Eight Decades of Data on Why the Best Investor Response Is Often No Response at All

“History has witnessed nine major geopolitical shocks since 1941. The S&P 500 was higher twelve months later in seven of them. The three exceptions share a common cause — oil. Everything else is noise.”

The 2026 Iran War: What Is Actually Different This Time

The war that began on 28 February 2026 is unlike any Middle Eastern conflict since the Yom Kippur War of 1973. Israel and the United States launched joint strikes targeting Iran’s nuclear infrastructure and ballistic missile programme, following the complete breakdown of diplomatic negotiations. Iran responded with a barrage of drones and ballistic missiles across the Gulf, triggering emergency sessions at the UN Security Council and sending oil prices to $112 per barrel within days.

For Australian investors, the immediate reaction was swift. The ASX 200 shed more than 8% from its March peak near 9,200, erasing year-to-date gains and prompting the kind of portfolio anxiety that precedes poor decisions. Phones are ringing. Emails are arriving at midnight. The question in every message is the same: Should I do something?

The honest answer — the one supported by 85 years of market data — is almost certainly no. But that answer requires evidence, not reassurance. What follows is that evidence.

S&P 500 Returns Under the Weight of Geopolitical Conflict, 1941–2026

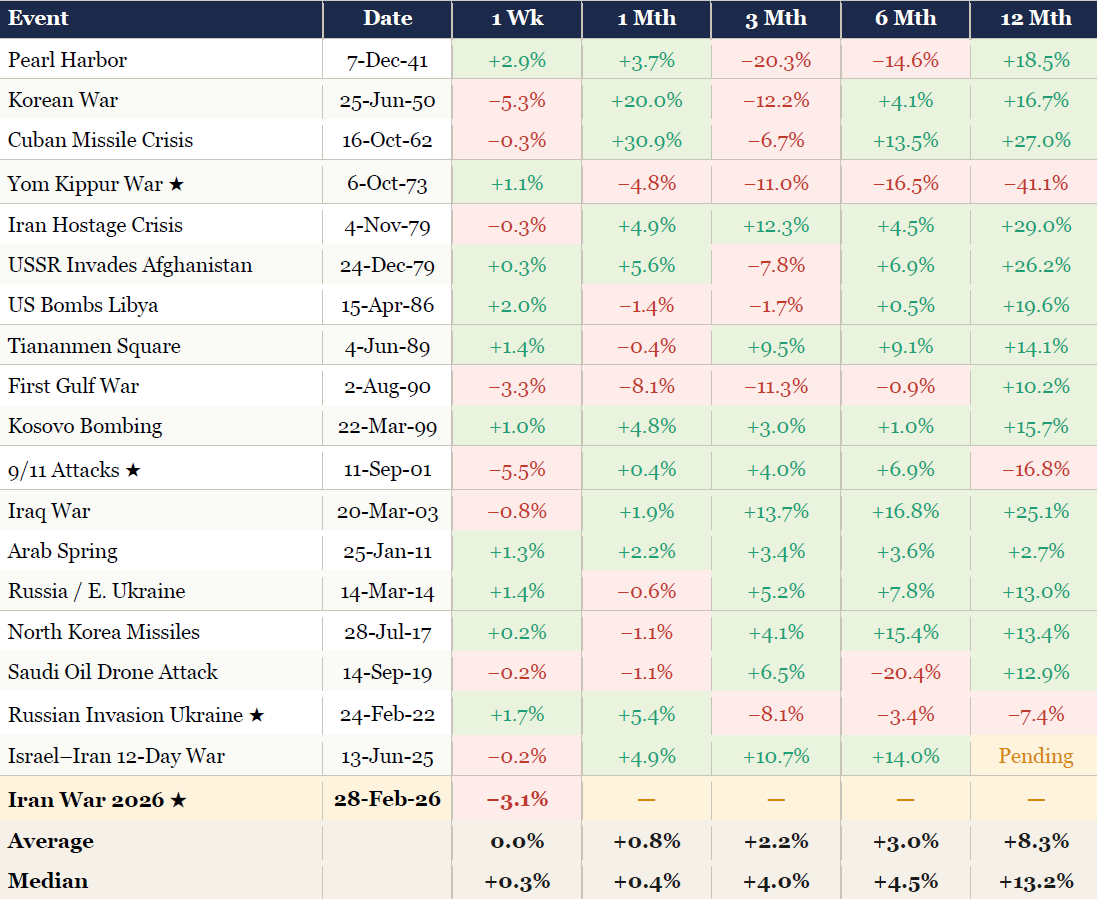

The table below extends the Ophir Asset Management / Bloomberg dataset to include conflicts from World War II onwards. The data covers 19 major events, cross-referenced across Bloomberg, LPL Research, First Trust Portfolios / Ken French Data Library, and AAII. Each row represents the S&P 500 return in the 1-week, 1-month, 3-month, 6-month, and 12-month windows following the onset of the conflict. ★ denotes events coinciding with oil shocks or recessions.

The pattern is unmistakable. Of the 18 resolved events in this dataset, 14 produced positive 12-month returns. The three events with negative 12-month returns — Yom Kippur 1973, 9/11, and Russia–Ukraine 2022 — each coincided with a prolonged oil shock, a pre-existing recession, or both. No other variable meaningfully predicts a sustained bear market following a geopolitical shock.

The Two Conditions That Separate a Correction from a Catastrophe

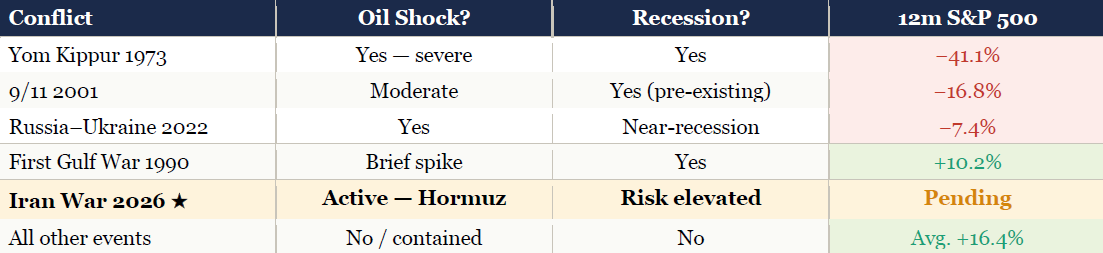

Not all geopolitical shocks are created equal. Eighty-five years of data across 19 major conflicts reveal a clean two-variable framework that separates recoveries from prolonged bear markets. The variable is not the size of the conflict, the number of casualties, or the geopolitical significance of the adversary. It is, almost entirely, oil.

Every event that produced a negative S&P 500 return over 12 months was accompanied by either a sustained oil price shock, an active U.S. recession, or both. The Yom Kippur War produced the Arab oil embargo — oil prices quadrupled within months, triggering stagflation and the worst bear market since the Great Depression. The aftermath of 9/11 combined geopolitical shock with a recession already underway from the dot-com bust. The Russia–Ukraine conflict of 2022 came with a global energy price shock that amplified already-elevated inflation, forcing the most aggressive central bank tightening cycle in forty years.

The 2026 Iran War therefore sits at a genuine crossroads. The Strait of Hormuz carries roughly one-fifth of global seaborne oil. A sustained closure would move the conflict from the ‘contained’ category into the 1973 scenario. This is the only variable that Australian investors should be watching — not the daily headline count, not the missile tallies, not the UN Security Council votes. The question is simple: does this conflict produce a persistent oil shock that reshapes inflation expectations and forces central banks to tighten beyond current pricing?

If the answer is no — if the strait remains open, GCC producers offset supply losses, and U.S. shale responds as it did in 2019 — the historical base case is recovery within months and positive returns within twelve. If the answer is yes, the calculus changes materially. But even in that scenario, the correct response is not selling equities. It is reviewing energy exposure, checking your cash buffer, and ensuring your portfolio’s duration risk is appropriate for an inflationary environment.

Does Conflict Duration Determine Market Outcomes?

One of the most persistent investor misconceptions is that longer conflicts produce worse market outcomes. The data does not support this. Vietnam lasted nearly eight years — the S&P 500 gained 43% during it. The Yom Kippur War lasted nineteen days — the market lost 41% over the following twelve months. The Korean War ran for three years and produced a 16.7% gain over its first twelve months despite initial sharp falls. Duration is not the variable. The economic consequences of the conflict are the variable.

The scatter of 12-month returns across all 19 events in our dataset shows no statistically meaningful correlation with conflict duration. What it does show is a clean clustering by economic consequence: events accompanied by oil shocks or recessions cluster in negative territory regardless of duration; all others cluster firmly positive, again regardless of duration. Investors who exited on the basis of ‘this one could last a long time’ paid a compounding price for a thesis that the data consistently refutes.

Why the Instinct to ‘Wait for Clarity’ Is a Wealth Destruction Engine

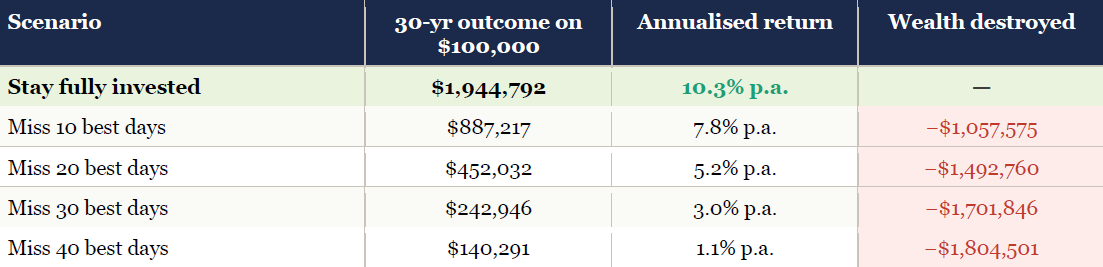

Every investor who moves to cash during a geopolitical shock faces the same problem: they must also decide when to re-enter. This second decision is, in every documented study of investor behaviour, made worse than the first. The mechanism is simple — by the time clarity arrives, the recovery has already happened. The gains from the rebound are precisely the gains that define long-run portfolio outcomes.

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

— Peter Lynch, Magellan Fund

The numbers above are not theoretical. They represent the actual wealth gap between an investor who holds through geopolitical noise and one who exits during a conflict and misses even a small number of the market’s best days. Note the timing of those best days: according to Hartford Funds and Ned Davis Research, 78% of the S&P 500’s best days occur during a bear market or in the first two months of a bull market. The investor who exits to ‘wait for clarity’ is almost mathematically certain to miss the very days that generate the majority of long-run wealth creation.

The DALBAR Quantitative Analysis of Investor Behaviour (2025) confirms this consistently: in 2024, the average equity fund investor underperformed the S&P 500 by 8.48% — the second-largest annual investor gap in a decade. The underperformance is not explained by fees or fund selection. It is explained entirely by poorly timed entries and exits.

The Answer to the Question Every Client Is Asking

The 2026 Iran War is the most significant Middle Eastern conflict in half a century. The humanitarian stakes are enormous. The geopolitical implications will reverberate for decades. None of that is in question. What is in question — the narrow question that guides portfolio construction — is whether this conflict will produce the sustained oil shock and recession that have historically been the prerequisite for a lasting equity bear market.

The base case, supported by 85 years of data and the structure of today’s energy markets, is that it will not. The U.S. is a net energy exporter in a way it was not in 1973. Saudi Arabia and the UAE have significant spare capacity and a strong incentive to deploy it. Global oil demand growth has been structurally declining for a decade. The 1973 scenario is not impossible — but it requires a sustained Hormuz closure, not merely a threat of one.

The median 12-month S&P 500 return following the 18 comparable conflicts in our dataset is +13.2%. The average is +8.3%. Of the three events that produced negative 12-month returns, every one involved either a recession that was already underway or a multi-month oil embargo. None of those conditions are currently present.

“The stock market is a device for transferring money from the impatient to the patient.” In 85 years of geopolitical shocks, that observation has been validated every single time.

— Warren Buffett

- Ophir Asset Management / Bloomberg — Israel–Iran 12-Day War (Jun 2025) and original conflict return table framework

- LPL Research / Bloomberg / FactSet / S&P Dow Jones Indices — geopolitical shock event study (2024)

- First Trust Portfolios / Ken French Data Library / CRSP — U.S. market-cap weighted returns, major wars and shocks (Q4 2024)

- AAII — S&P 500 peak drawdowns and recovery timelines, 17 post-WWII events

- A Wealth of Common Sense (B. Carlson) — historical conflict return data, WWII through Ukraine 2022

- Hartford Funds / Ned Davis Research / Morningstar — market timing cost analysis, 30-year best-days study (Feb 2025)

- Wells Fargo Investment Institute — Perils of Timing Volatile Markets (Jul 2025)

- DALBAR — Quantitative Analysis of Investor Behavior (2025)

- J.P. Morgan Private Bank — 80+ years of geopolitical shock analysis (2024)

- Al Jazeera / ABC News / UK Parliament Briefing CBP-10521 — 2026 Iran War facts and timeline