2026–27 Federal Budget: What Every Australian Investor Must Know Now

1. Capital Gains Tax: The Most Significant Overhaul Since 1999

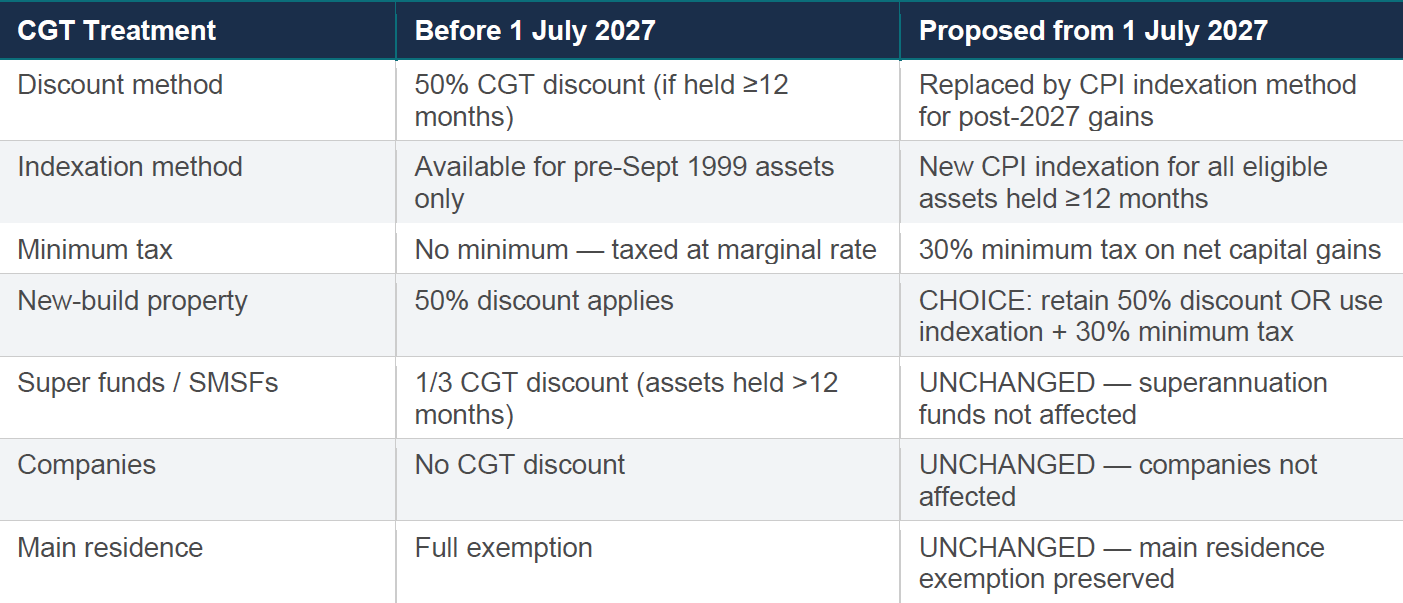

The 2026–27 Federal Budget delivers the most sweeping reform to capital gains tax (CGT) since the Howard government introduced the 50% discount in 1999. From 1 July 2027, that discount is proposed to be replaced for most taxpayers by CPI-based indexation and a hard minimum 30% tax floor. These are Budget proposals that require separate legislation to become law; however, they carry a strong Government mandate following its 2025 election majority. Note: these measures do NOT yet apply — they are proposals only.

What Is Proposed to Change

The Transitional Rules — Critical for Long-Term Holders

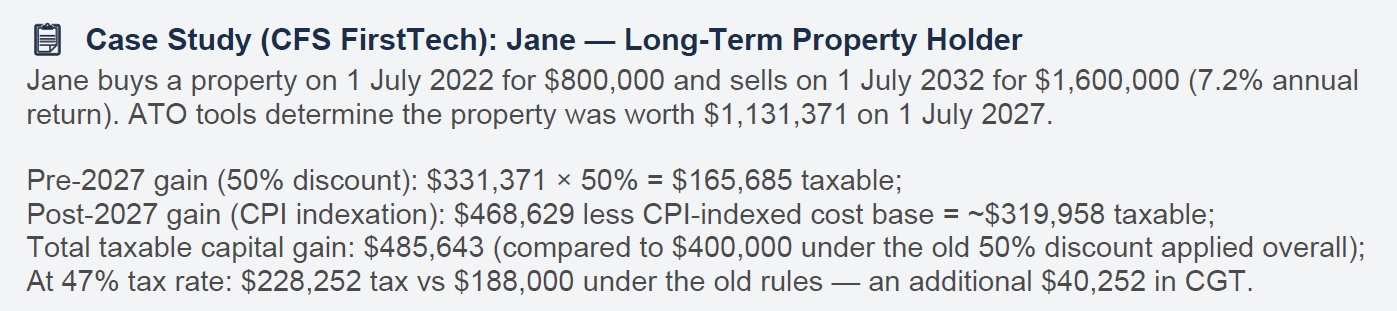

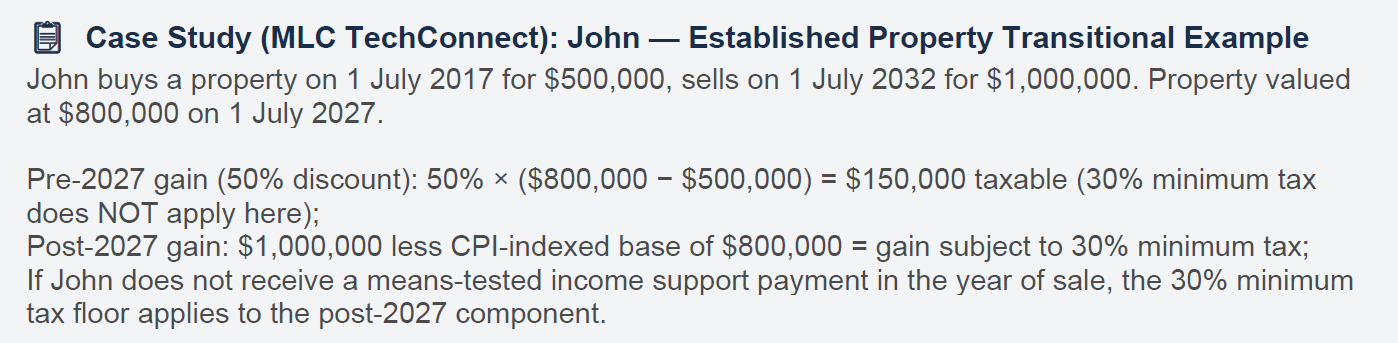

For assets bought before 1 July 2027 and sold after that date, the Government has confirmed a split-calculation approach. Gains accrued up to 30 June 2027 are treated under current rules — meaning the 50% discount still applies to the pre-2027 portion. Gains accruing from 1 July 2027 onward are assessed under the new CPI indexation method with the 30% minimum tax applied.

Taxpayers will need to determine the value of their CGT asset as at 1 July 2027 either by obtaining a formal valuation or using an ATO apportionment formula tool. This valuation step will be required in the tax return for the year the asset is eventually sold.

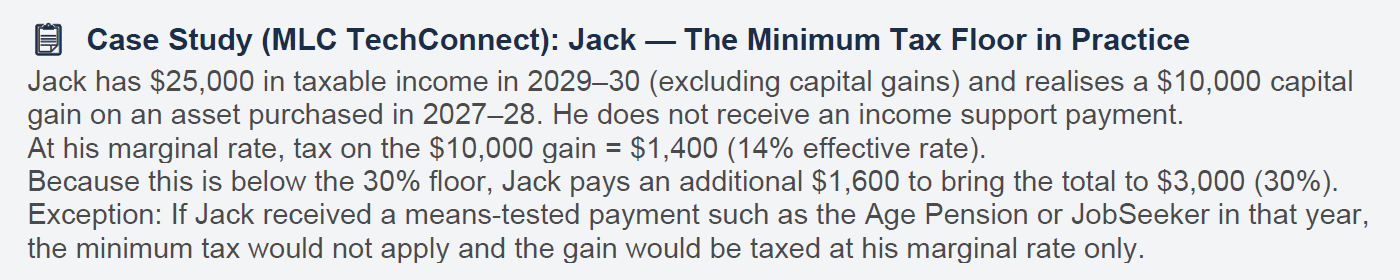

The 30% Minimum Tax: Who Is Affected

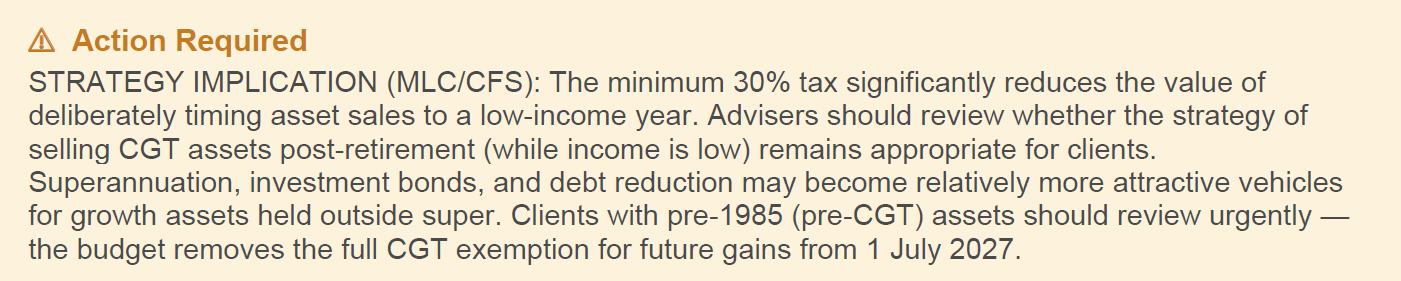

The 30% minimum tax is designed to prevent the strategy of selling CGT assets in low-income years — for instance, after early retirement — to reduce the effective tax rate on gains. Under the new rules, even a retiree with minimal other income will pay at least 30% on net capital gains accruing from 1 July 2027.

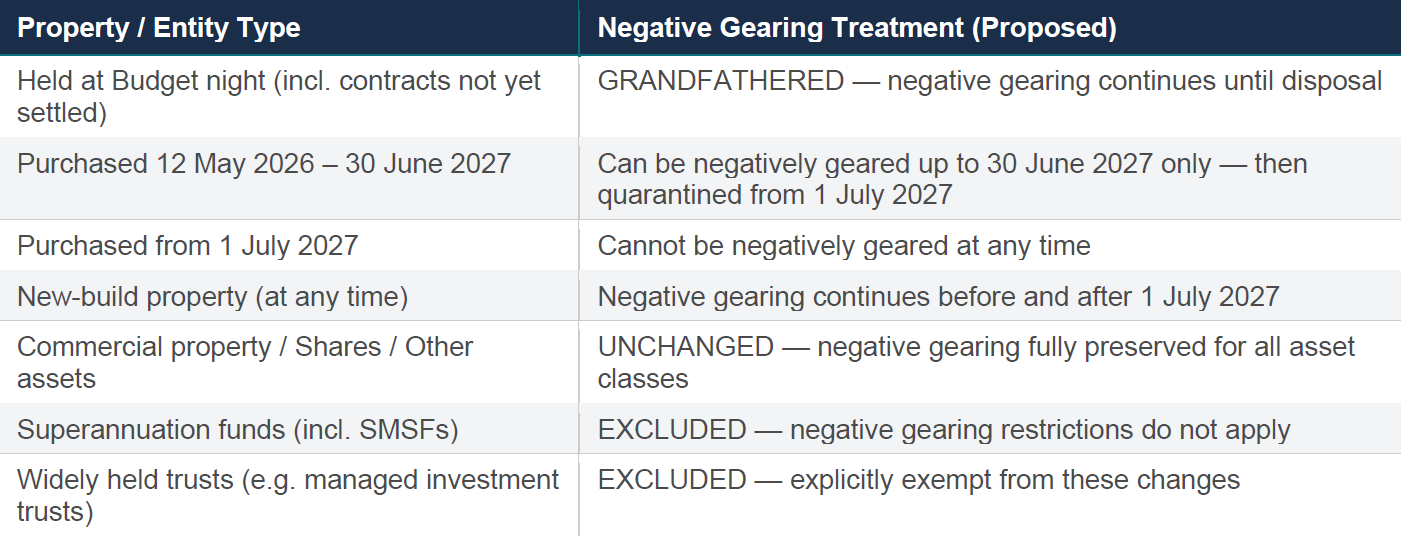

2. Negative Gearing: PROPOSED Restriction to New Builds from 1 July 2027

The Government has proposed to restrict negative gearing on established residential properties for properties acquired on or after Budget night — 7:30pm AEST, 12 May 2026. These are proposals only and require separate legislation to become law. From 1 July 2027 (if legislated), losses from these properties cannot be offset against other income such as salary. The losses would be ring-fenced: they can only be applied against future residential property income (including capital gains on disposal).

These changes apply to individuals, partnerships, companies and most trusts. Explicitly excluded are: superannuation funds (including SMSFs), widely held trusts (such as most managed investment trusts), and commercial property and other non-residential asset classes such as shares.

Timeline and Transitional Rules

What Qualifies as a 'New Build'?

The Government has defined new-build properties narrowly to ensure the concession genuinely supports housing supply:

• Dwellings constructed on vacant land

• Properties where existing structures are demolished and replaced with a greater number of dwellings

• The property must not have been previously sold, unless originally owned by the builder and occupied for no more than 12 months

• Subsequent purchasers of a new-build dwelling cannot access the negative gearing concession

Knock-down rebuilds and substantial renovations that do not increase housing supply do not qualify as new builds.

Impact on Multi-Property Investors

Unlike the original two-property cap proposals that were modelled before the Budget, the final announcement goes further: all established residential properties acquired from Budget night will be unable to be negatively geared — regardless of how many properties an investor holds. There is no per-investor limit; instead, the restriction is based on property type and acquisition date.

Losses that are carried forward remain available to offset future residential property income — and importantly, CFS FirstTech's analysis notes that unused losses at the time of a property's sale would likely be added to the property's cost base, thereby reducing the gross capital gain on disposal.

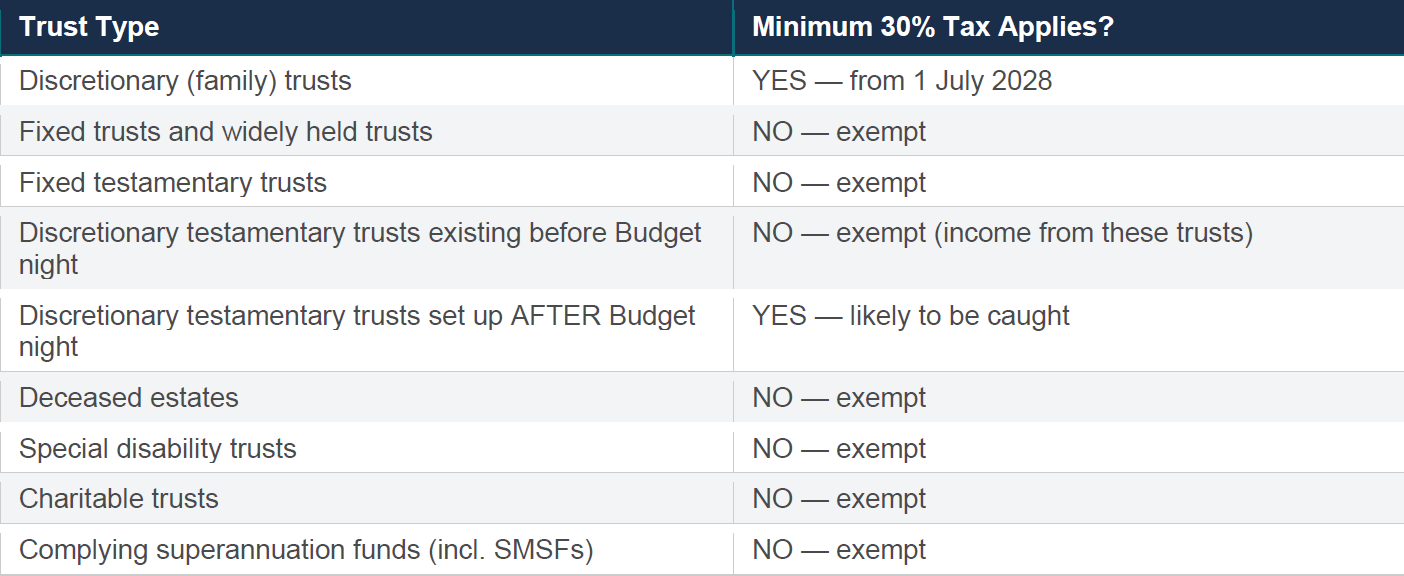

3. Discretionary Trusts: 30% Minimum Tax from 1 July 2028

A minimum 30% tax rate will be applied to the taxable income of discretionary trusts from 1 July 2028. This closes the long-standing strategy of distributing trust income to low-income beneficiaries, including adult children and spouses with minimal other income, to reduce the overall family tax burden.

How It Works

The trustee pays the minimum 30% tax on the trust's taxable income (broadly: assessable income less allowable deductions). Beneficiaries other than corporate beneficiaries then receive a non-refundable tax credit for the tax paid by the trustee. This means beneficiaries with a marginal rate above 30% face no additional impost — but those on lower rates no longer receive distributions taxed at their personal marginal rate.

Corporate beneficiaries (bucket companies) will not receive non-refundable credits — a deliberate design to prevent the minimum tax being avoided by distributing to a company and then accessing refundable franking credits.

Exemptions — Not All Trusts Are Affected

Rollover Relief for Restructuring

To assist small businesses and families who need to exit discretionary trust structures, the Government will provide expanded rollover relief — including for CGT purposes — for three years from 1 July 2027. This allows restructuring into a company or fixed trust without immediate CGT consequences.

4. Superannuation: Budget Confirms Already-Legislated Reforms

There were no new superannuation measures in the 2026–27 Budget. However, the Budget formally acknowledges — and funds the administration of — two major changes already passed into law and taking effect from 1 July 2026. Both require immediate action from affected fund trustees and members.

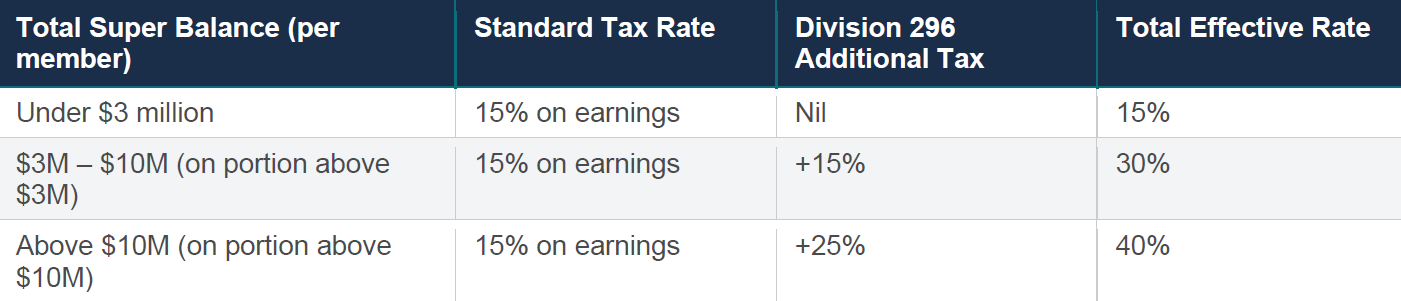

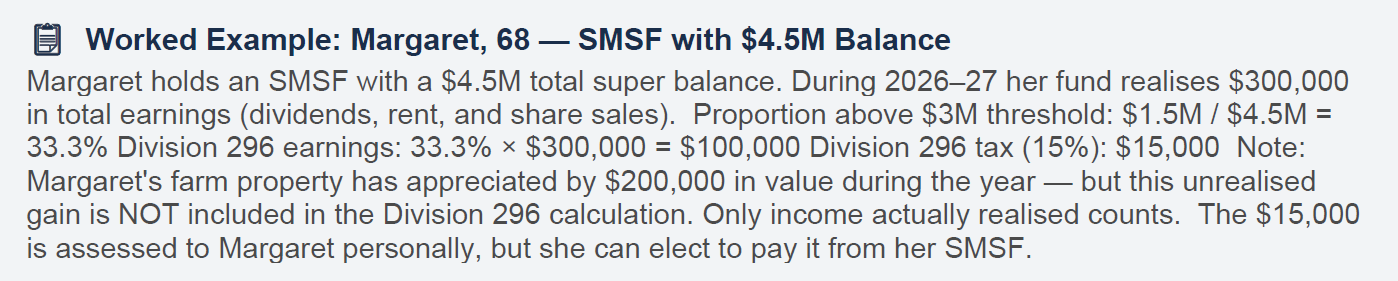

Division 296: The New Tax on Large Super Balances — Now Law

Critical features of the final legislation: the tax applies only to REALISED earnings — dividends, interest, rent, and capital gains crystallised during the year. Unrealised gains (paper appreciation) are explicitly excluded. Both thresholds are indexed annually ($3M threshold in $150,000 increments; $10M threshold in $500,000 increments). The Division 296 tax is a personal tax assessed to the individual — but can be paid from the super fund.

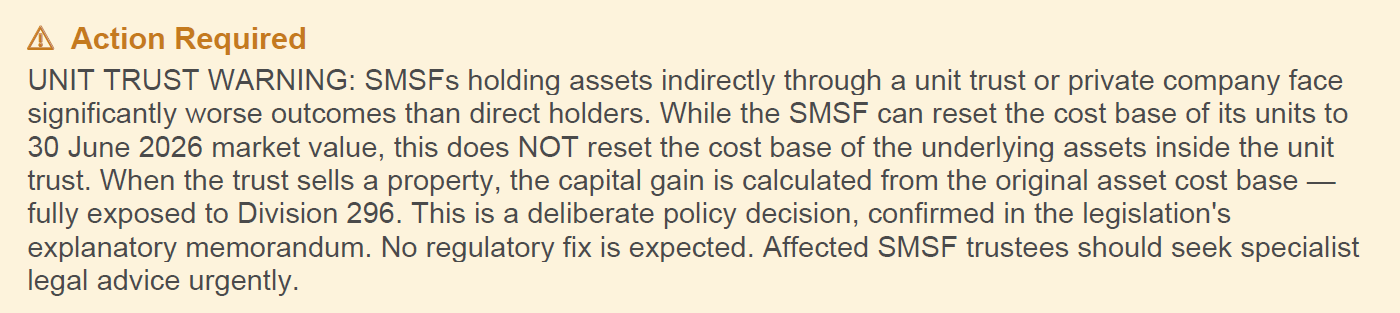

Cost-Base Reset Election — SMSFs Only, Critical Deadline

SMSFs have a one-time opt-in available: they can elect to reset the cost base of all CGT assets to market value at 30 June 2026, so that capital gains accrued before Division 296 commenced are excluded from future assessments. This election applies at fund level — all assets are included, even those in unrealised loss positions.

Payday Super: Also Now Law — 1 July 2026

For SMSF trustees, this means contribution deposits arrive on every pay cycle rather than quarterly. Investment strategy documents should be reviewed to ensure they reflect this higher-frequency liquidity environment. For employees, super balances will compound more rapidly as contributions are invested sooner.

Contribution Caps & Transfer Balance Cap — Legislated Increases from 1 July 2026

LISTO Increase — Legislated for 1 July 2027

5. Personal Income Tax Relief: Cuts, a New Offset & Instant Deductions

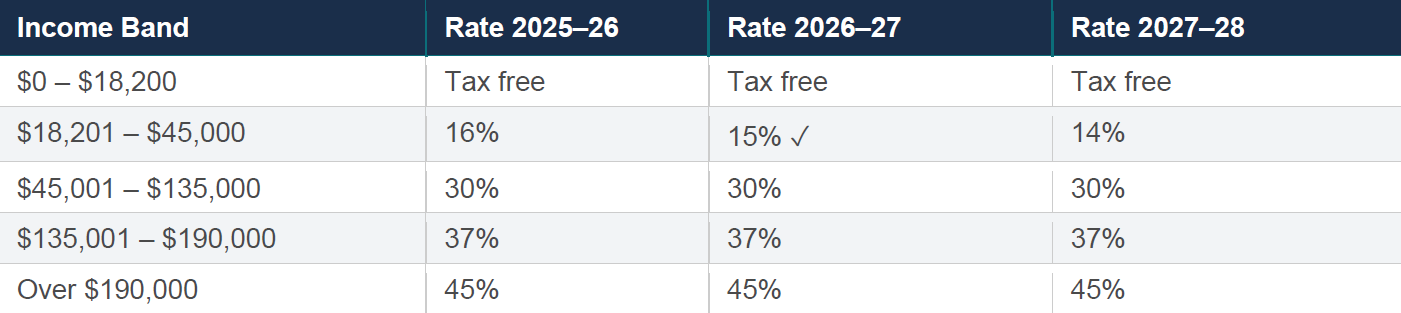

Stage 3 Phase 2 Tax Cuts — Already Law

$1,000 Instant Tax Deduction for Work-Related Expenses — From 1 July 2026

From the 2026–27 income year, eligible Australian tax residents who earn income from work can claim an automatic $1,000 deduction for work-related expenses without keeping receipts. Those with work-related expenses above $1,000 can opt out and claim their full expenses in the usual way (with substantiation).

Importantly, charitable donations, union and professional association memberships, and other non-work-related deductions can still be claimed separately, in addition to the $1,000 instant deduction.

Working Australians Tax Offset (WATO) — Proposed from 1 July 2027

The Government proposes a permanent $250 non-refundable tax offset from 2027–28, applying to income derived from work (wages, salaries, and sole trader business income). The WATO is not means-tested and is available regardless of age. Combined with the already-legislated tax cuts, it lifts the effective tax-free threshold for workers to approximately $19,985 (or up to $24,985 for those also eligible for the Low Income Tax Offset).

6. Other Key Budget Measures

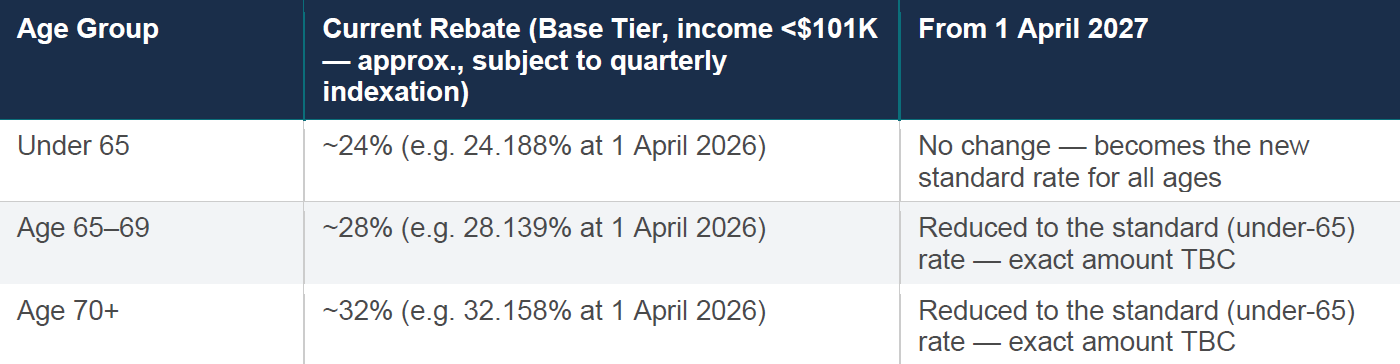

Private Health Insurance Rebate — Age-Based Uplift Removed from 1 April 2027

The Government will remove the age-based uplift in the private health insurance (PHI) rebate from 1 April 2027, saving approximately $3 billion over four years. Currently, policyholders aged 65–69 receive a rebate roughly 4 percentage points higher than those under 65, and those aged 70+ receive a rebate roughly 8 percentage points higher. From 1 April 2027, all ages will receive the same base rebate percentage — meaning older Australians face a direct increase in premiums. Note: rebate percentages are indexed quarterly and the exact figures that will apply from 1 April 2027 have not yet been confirmed.

Business: $20,000 Instant Asset Write-Off Made Permanent

The $20,000 instant asset write-off threshold for small businesses (turnover under $10 million) will be made permanent from 1 July 2026, removing the uncertainty around annual renewals. Assets valued at $20,000 or more continue to be placed into the simplified depreciation pool (15% in year 1, 30% thereafter). The five-year exclusion on re-entering the simplified depreciation regime after opting out remains suspended until 30 June 2027.

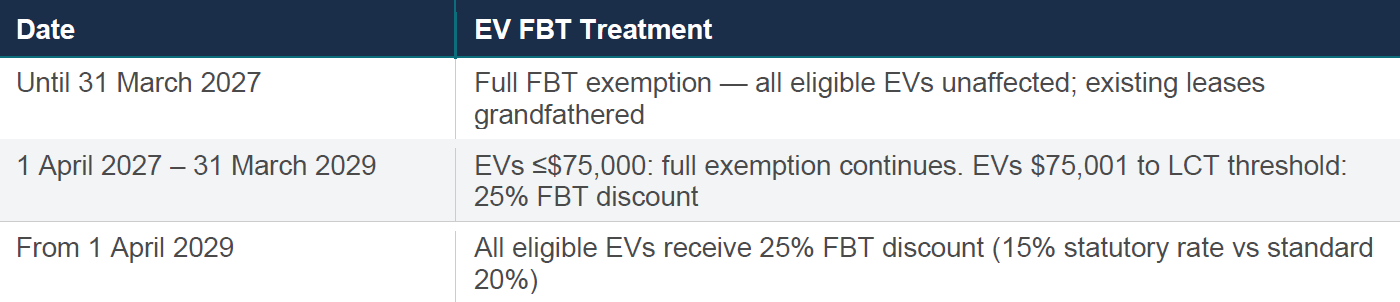

Electric Vehicle FBT Concessions — Progressive Wind-Down from April 2027

7. Aged Care & Social Security

Aged Care: Supply, Home Support & Pension Overseas Rules

The 2026–27 Budget continues significant investment in aged care infrastructure and access, building on the reforms commenced in prior years:

• 5,000 additional residential aged care beds per year, incentivised through building subsidies and a restructured Accommodation Supplement (from 1 July 2026)

• Personal care services (showering, dressing, incontinence aids) reclassified as clinical care from 1 October 2026 — becoming fully government-funded for all Support at Home recipients

• Faster access to Support at Home places with improvements to assessments, hardship applications and the end-of-life pathway

• Additional dementia care funding, including expansion of the Hospital to Aged Care Dementia Support program

On the Pension Supplement, from 20 September 2026, recipients temporarily overseas will receive the full supplement for 12 weeks (up from 6 weeks) — but the supplement will cease entirely after 12 weeks of absence or upon permanent departure overseas. Age Pensioners who retire abroad permanently will no longer receive the Pension Supplement basic amount, which was previously paid indefinitely.

Centrelink Context: Deeming and Assets Test (Already Effective March 2026)

While not a Budget measure, the March 2026 Centrelink changes — including a 0.5 percentage point increase in deeming rates — continue to affect investor strategies. The current deeming rates are 1.25% on financial assets up to $64,200 (singles) / $106,200 (couples), and 3.25% above those thresholds.

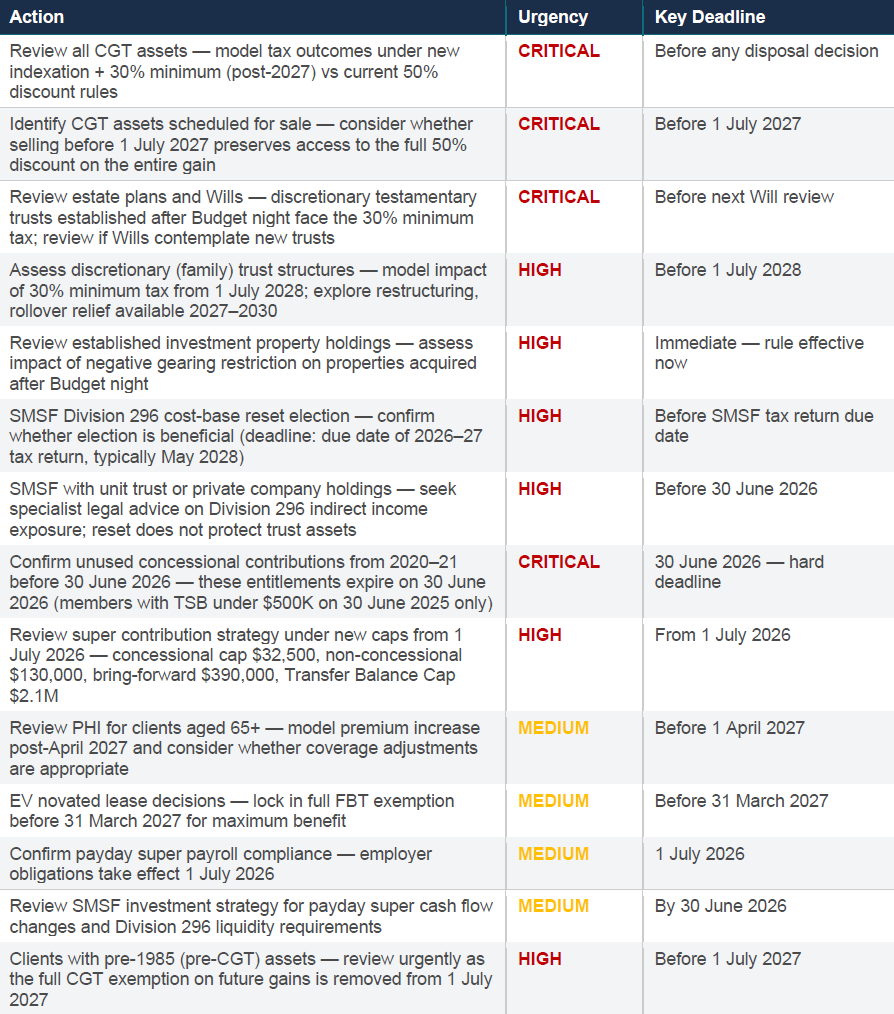

8. The 2026 Budget Investor Action Checklist

"The 2026–27 Budget marks the most consequential proposed shift in the Australian tax and investment landscape in a generation. The proposed replacement of the 50% CGT discount, the restriction of negative gearing to new builds, the discretionary trust minimum tax, and the already-operational Division 296 superannuation levy together signal a fundamental rewrite of the rules of wealth accumulation in Australia. Several of these measures are proposals only — but investors and advisers who model outcomes now and restructure where warranted will hold the initiative. Those who wait for certainty may find the landscape has already shifted beneath them." — The Long View, May 2026

CFS FirstTech Federal Budget 2026–27 Briefing Paper (12 May 2026); MLC/Expand Federal Budget 2026 Adviser Analysis (12 May 2026). All figures and examples are for illustrative purposes. These changes are proposals only and may not all be enacted as law.

This communication is for informational purposes only and does not constitute financial, legal or tax advice. Individuals must not rely on this information to make a financial or investment decision. Before acting, consult a licensed financial adviser, registered tax agent or solicitor regarding your specific circumstances.