2026 Tax, Super & Centrelink — Part I: Superannuation Reforms & Strategic Implications

"The rules governing how Australians save, invest, and retire are changing more rapidly in 2026 than at any point in the past two decades. Complacency is the greatest risk."

The calendar year 2026 marks a watershed moment in Australian retirement and investment policy. The Albanese government's sweeping reforms to superannuation, the indexation of Centrelink thresholds, new deeming rates, and the looming spectre of capital gains and negative gearing reform ahead of the May 2026 Federal Budget have created an environment in which doing nothing is itself a strategic choice — and quite possibly the wrong one. This briefing sets out, with precision and examples, what has changed, what is coming, and what prudent investors should be doing now.

Super Under the Knife: The Division 296 Tax and Payday Super

From 1 July 2026, Australian superannuation is entering a new era of tiered taxation. Two landmark changes arrive simultaneously — one targeting high-balance accounts, the other transforming how employers pay contributions. Neither is optional. Both require action.

Division 296: The New Super Tax on Large Balances

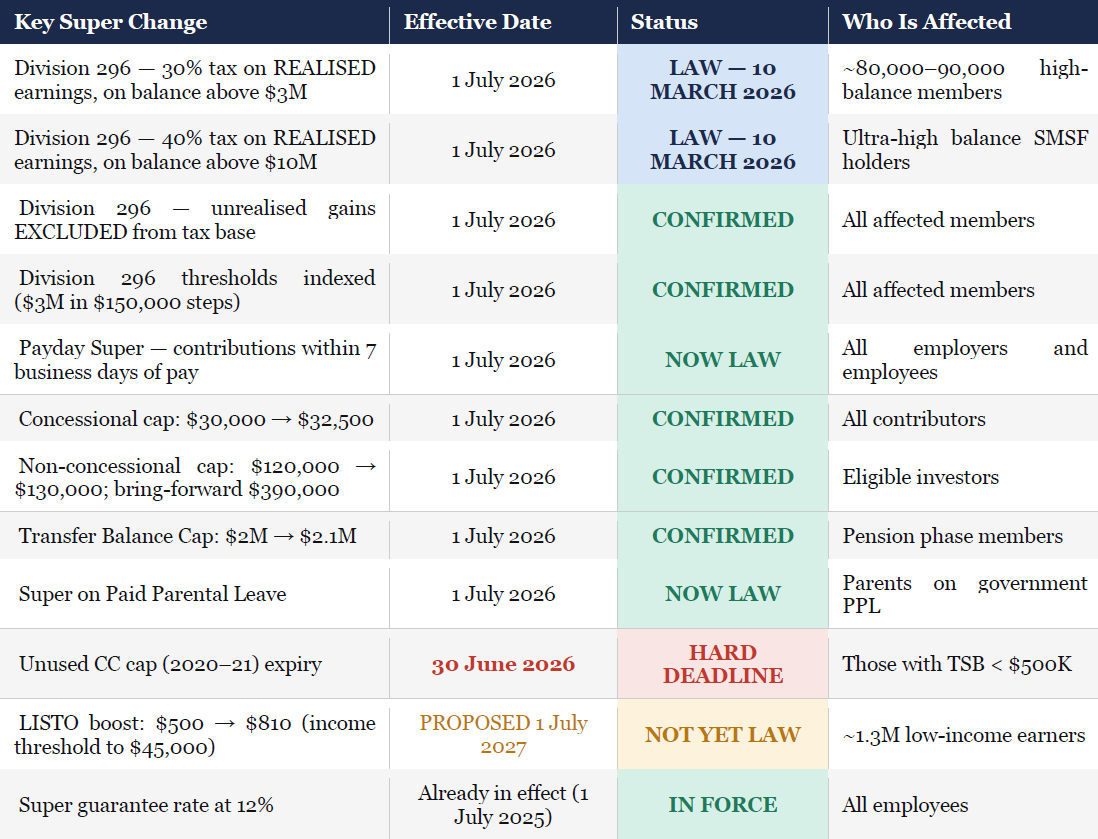

The Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026 passed both houses of Parliament on 10 March 2026 and takes effect 1 July 2026. The final legislation differs substantially from the original 2023 proposal: following sustained industry criticism, Treasury revised the tax base away from a balance-movement method that captured unrealised gains to a realised earnings approach. The law taxes only dividends, interest, rent, and realised capital gains — paper appreciation in asset values is excluded entirely.

Both thresholds will be indexed annually (the $3M threshold in $150,000 increments; the $10M threshold in $500,000 increments), addressing the original legislation's most-criticised feature — fiscal drag that would have captured a growing share of Australian savers over time. The Division 296 tax is a personal tax assessed to the individual, not to the super fund, though it can be paid from the fund.

"The original proposal would have taxed unrealised gains — paper profits on assets not yet sold. The final law dropped this entirely. Only realised earnings count: dividends, interest, rent, and capital gains actually crystallised during the year."

Who Is Affected and How Is It Calculated?

The government estimates approximately 80,000–90,000 Australians will be directly affected. The ATO notifies the super fund when a member's TSB exceeds $3 million; the fund then calculates and reports realised earnings attributable to that member. Division 296 tax is then applied to the proportion of those earnings corresponding to the member's balance above the relevant threshold.

Importantly, where assets have been held for more than 12 months, the standard one-third CGT discount continues to apply within the Division 296 calculation. If a member has negative earnings in a given year, the Division 296 assessment is nil — and those negative earnings do carry forward to reduce Division 296 earnings in future years. This is an important protection for SMSF members holding assets with volatile returns such as growth shares or property, where a loss year can offset a future gain year.

Worked Example: Margaret, 68, holds an SMSF with a $4.5 million TSB. During 2026–27 her fund realises $300,000 in total earnings (dividends, rent, and the sale of some shares). The proportion of her balance above $3M is $1.5M / $4.5M = 33.3%. Division 296 applies to 33.3% of $300,000 = $100,000. The additional 15% Division 296 tax = $15,000 — assessed to Margaret personally, payable from her fund if she elects. The farm property's unrealised appreciation is not included in this calculation — only income actually realised counts.

Payday Super: From Quarterly to Every Payday

From 1 July 2026, all employers must pay superannuation guarantee (SG) contributions within seven business days of paying salary and wages. This replaces the existing regime that allowed quarterly payment — a system that has, in practice, left workers at risk when employers run into financial difficulty. The ATO estimates $3.4–$6.25 billion in super goes unpaid annually under the current regime.

Workers will see super credited to their fund far more frequently, accelerating the compounding of investment returns. Employers who pay late will face additional charges and may breach the Fair Work Act. For SMSF trustees managing cash flow projections, contribution timing will become more predictable. Payday super also changes SMSF cash management — from July 2026 the fund receives deposits on every pay cycle. Trustees should update their investment mandates to reflect this higher-frequency liquidity environment.

Low-Income Super Tax Offset (LISTO): Proposed Enhancement

The Division 296 bill also includes a proposed boost to the Low-Income Super Tax Offset. From 1 July 2027 (not 2026 — this is a proposed change not yet passed), the maximum LISTO is proposed to increase from $500 to $810, and the income eligibility threshold from $37,500 to $45,000. This has not yet been legislated and requires separate parliamentary approval. If passed, Treasury estimates it will benefit approximately 1.3 million low-income Australians, many of them women.

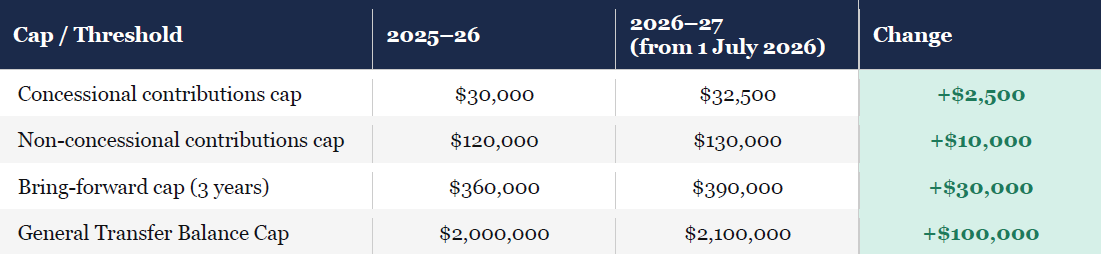

Contribution Caps Increase from 1 July 2026

From 1 July 2026, contribution caps increase for the first time since 2024. The concessional contributions cap rises from $30,000 to $32,500; the non-concessional cap rises from $120,000 to $130,000; and the bring-forward cap increases to $390,000. The general Transfer Balance Cap also rises from $2 million to $2.1 million, lifting related thresholds across non-concessional eligibility and co-contribution access.

Unused concessional contribution (CC) cap amounts from 2020–21 will expire if not used by 30 June 2026. Investors with a Total Superannuation Balance below $500,000 on 30 June 2025 who have unused CC space from prior years should act immediately with their adviser to capture these expiring entitlements.

Key Super Changes — Status Summary

• ATO — Better Targeted Superannuation Concessions (Division 296) guidance, January 2026

• SBS News — Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026 passage, March 2026

• Services Australia — Age Pension income and assets test thresholds, 20 March 2026

• Wealth Copilot — Age Pension Changes March 2026 analysis

• Hudson Financial Planning — The Super Sweet Spot (March 2026) and ATO Holiday Home Negative Gearing ruling

• Paris Financial — 2026 Super and Tax Changes overview

• HLB Mann Judd — Division 296 SMSF Changes, December 2025

• Finance Directory — Negative Gearing and CGT Changes 2026

• Property Investment Professionals — Negative Gearing Cap & CGT Changes 2026 Investor Guide

• The Senior / SBS News — 2026 Money Changes summary, January 2026

• Property Council of Australia — submission opposing CGT and negative gearing reform

• Senate Inquiry into CGT Discount — Final Report, March 2026

• DuoTax — Superannuation Tax Changes 2026 overview

• SMS Magazine — Sladen Legal / Phil Broderick analysis: Division 296 and indirect asset income, February 2026

• TAMIM Asset Management — Super Tax Reforms and SMSF Trustee implications, October 2025

• Boa & Co. Chartered Accountants — Super Tax Overhaul 2026: The $3M Rule for SMSF Trustees

• SMSF Wiz — Complete Guide to SMSF Property Investment 2026

• Citadel Agency — SMSF Property Rules 2026: What You're Allowed to Buy

• BDO Australia — 2026–27 Federal Budget preview and pre-budget submission

• CBA Economics — Housing Forecasts 2026 (CGT discount and property price modelling)

• Westpac Economics — Big Banks Diverge on Housing Forecasts, March 2026

• Grant Thornton Australia — Division 296: Key Elements of the New Legislation, March 2026

• ATO — Medicare Levy Surcharge income thresholds and rates 2025–26

• ATO — Crypto assets and tax: SMSF reporting obligations 2026

• ASIC MoneySmart — Death benefit nominations and super estate planning

• MLC / Superguide — Division 296 cost-base reset election: what trustees need to know

• Australian Aged Care Quality and Safety Commission — Aged care means testing overview

• Buyers Agency Australia — Negative Gearing 2026 analysis