The Guarantee Illusion, and the Case for Probability

Clients don’t ask for guarantees because they misunderstand risk — they ask because certainty feels safer than probability. The adviser’s job is to redirect that instinct, not dismiss it, and to show what a genuine “near-certainty” actually looks like across public and private markets.

Almost every investor, at some point, wishes for a product that delivers strong returns with no chanceof loss. It is not naivety — it is ordinary human psychology. Behavioural economics identifies a specific driver called the certainty effect: people consistently overvalue guaranteed outcomes relative to probable ones, even when the probable outcome is objectively better on average. Add loss aversion — a loss feels roughly twice as painful as an equivalent gain feels good — and it becomes clear why the word “guarantee” exerts such a powerful pull, particularly on retirees and conservative investors who feel they have less time to recover from a setback.

The uncomfortable truth is that genuine guarantees are extremely narrow. In Australia, the only broadly comparable protection is the Financial Claims Scheme, which covers deposits at authorised deposit-taking institutions up to $250,000 per account-holder per institution — and even that is a government guarantee on a bank deposit, not on an investment return. Beyond cash and government bonds held to maturity, no legitimate investment can guarantee a return, because return is the market’s compensation for risk. An offer to eliminate that risk while preserving the return is not a product innovation — it is a mathematical impossibility, and it is the single most common lure used in investment fraud.

"Investing is a probability calculation, not a coin toss — and the single biggest lever an investor controls is time."

What Comes Closest to a Guarantee: Time

Why longer holding periods have historically compressed the range of outcomes toward a near-certain positive result.

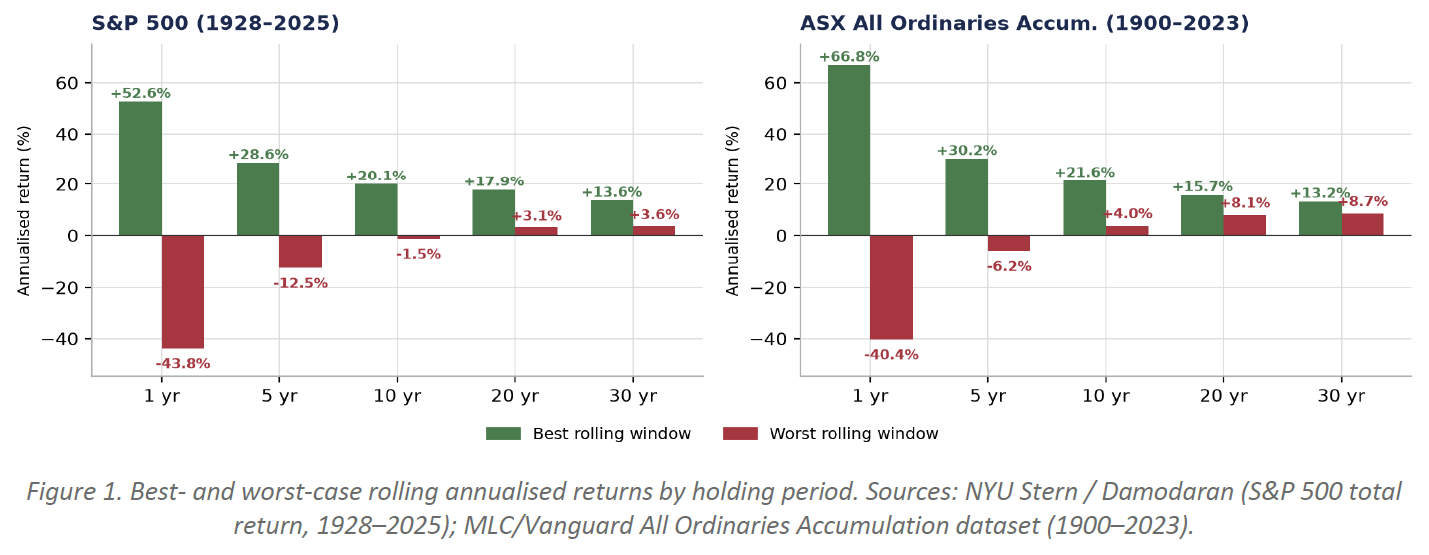

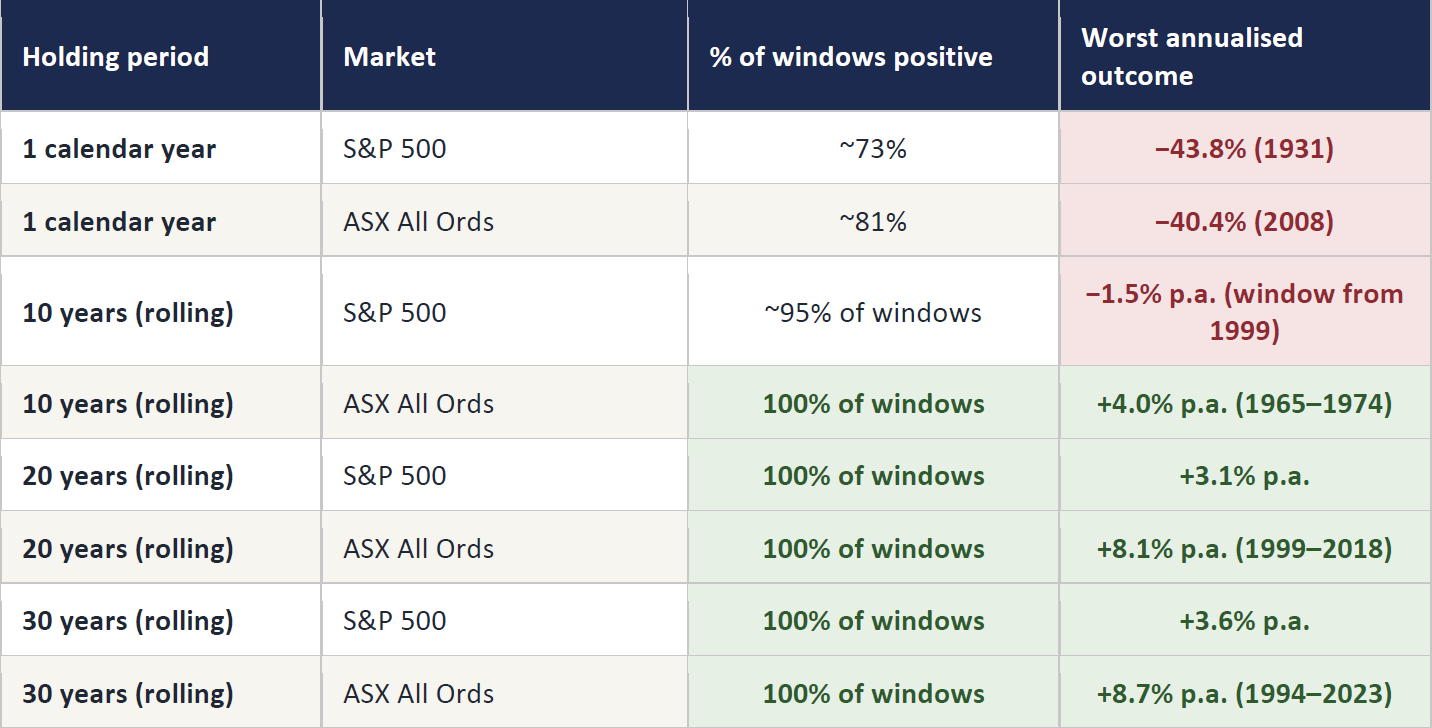

If a genuine guarantee is not available from a growth asset, the closest legitimate substitute is time. The chart below shows the range of rolling annualised returns for two of the world’s most widely held equity benchmarks — the S&P 500 (1928–2025) and the Australian All Ordinaries Accumulation Index (1900–2023) — at holding periods from one year out to thirty. What is striking is not the best cases (which everyone remembers) but the worst cases: as the holding period lengthens, the range collapses toward a positive floor.

The Australian market has, in this dataset, never produced a negative rolling 10-year return — a stronger result than the equivalent US figure, where the worst 10-year window (starting 1999) was mildly negative. Every rolling 20- and 30-year window in Australia’s history has returned at least 8% per annum. Over the past 30 years, Australian shares have averaged roughly 9.8% per annum despite absorbing the dot-com crash, the GFC and COVID-19. This is not a promise about the future, and the pre-1980 portion of the Australian dataset uses methodology the data provider itself flags as less reliably comparable — but it is a genuine, sourced, multi-generational pattern, which is precisely what no fraudulent “guarantee” product can ever offer.

INVESTOR TAKEAWAY

This is the honest version of what you are really asking for when you ask for a guarantee. It comes with two conditions no scam product ever has: a genuinely long time horizon, and the acceptance that any single year — including possibly the current one — can still be sharply negative.

Private Markets: Probability, Rewired

Time still matters — but through vintage diversification and manager selection rather than simply “holding on.”

Private markets don’t offer the same simple relationship between time and certainty, because there is no daily price and no ability to “wait out” a downturn by holding an index. Instead, probability is shaped by two separate levers: where you sit in a fund’s lifecycle (the J-curve), and how well-diversified your commitments are across vintage years and managers.

The J-curve: early losses are structural, not a warning

Private equity and venture capital funds typically show negative interim returns in their first two to four years, as management fees and early write-downs are recognised before portfolio companies mature and exit. This is a feature of how the asset class reports, not a sign a fund is failing.

INVESTOR TAKEAWAY

If your private-markets statement shows a loss in year two, you are not necessarily looking at a failing investment — more often you are looking at a textbook J-curve. Understand this before you commit capital, not after the first statement lands.

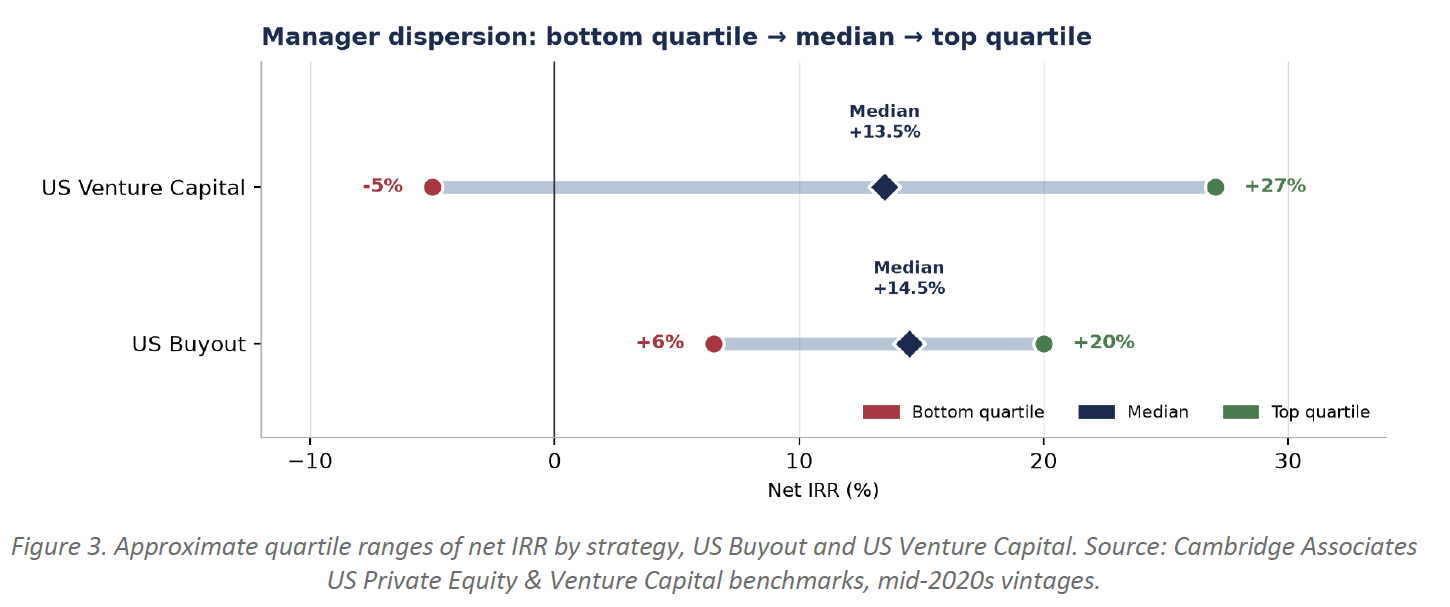

Manager selection and vintage diversification do the real work

Unlike public index investing, private markets returns vary enormously by manager. Cambridge Associates benchmark data (as of 2023) puts the spread between bottom- and top-quartile funds in a wide band — and the venture capital spread is roughly three times wider than buyout.

Venture capital dispersion is wider than buyout because VC returns follow a power law: in a typical fund of 20–30 portfolio companies, one to three investments generate 50–80% of total fund returns. This is precisely why manager selection, and diversification across vintage years, matter more in private markets than the simple passage of time.

INVESTOR TAKEAWAY

In private markets, “probability improves with time” means committing across multiple vintages and managers — not simply holding one fund for longer. Diversification is what substitutes for the liquidity a public index would otherwise give you.

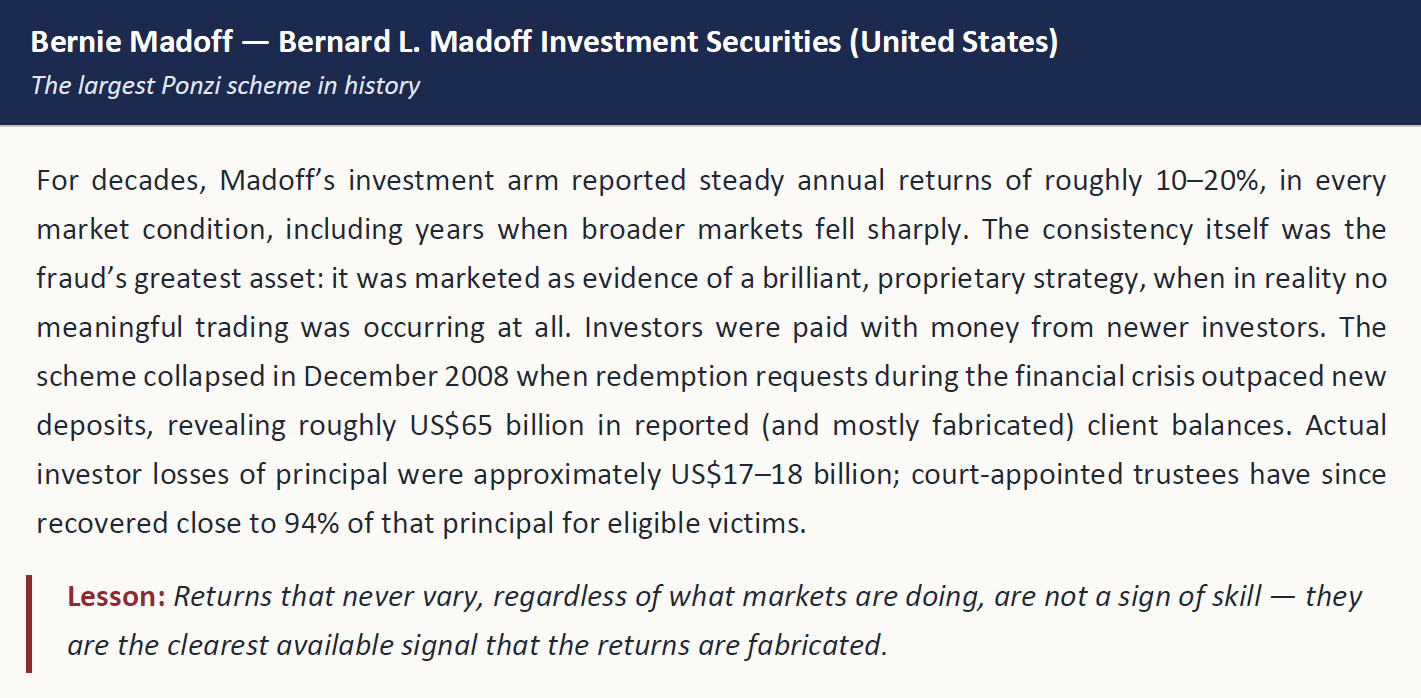

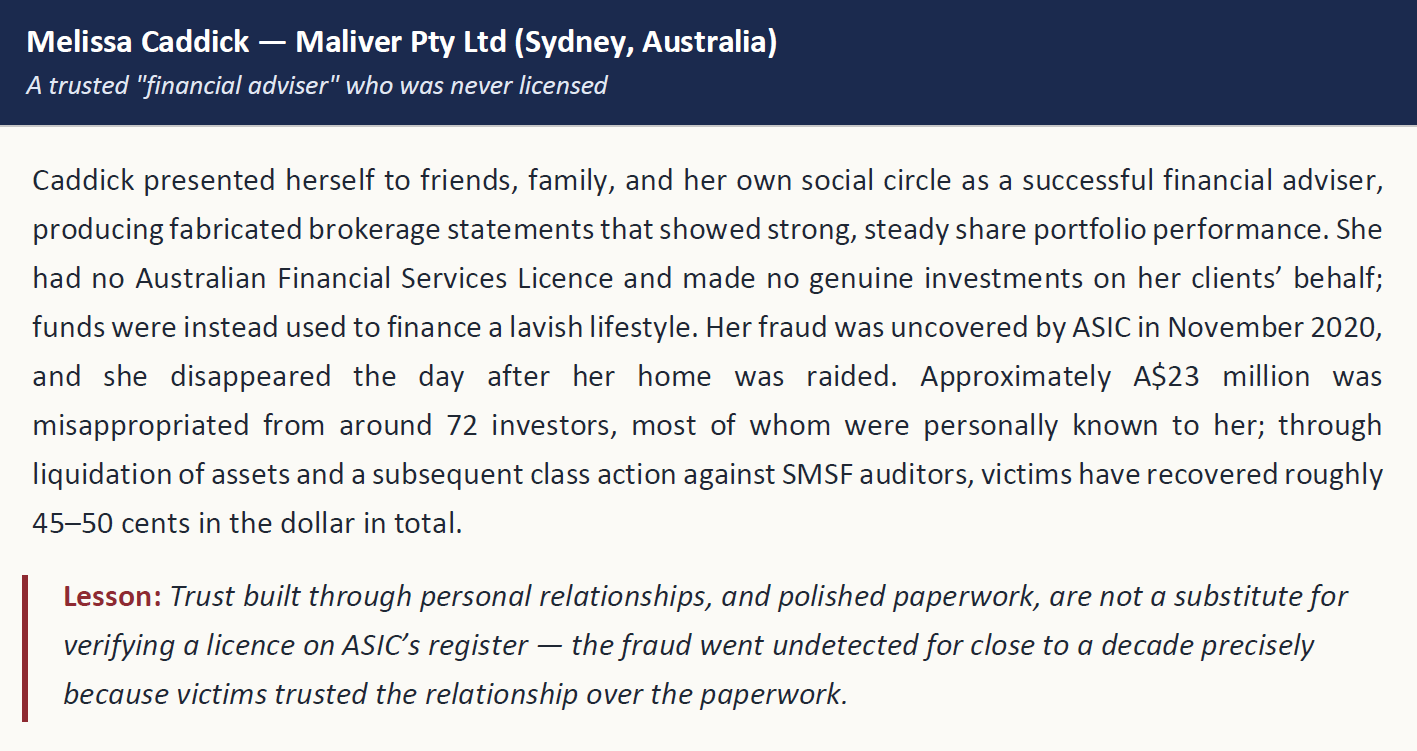

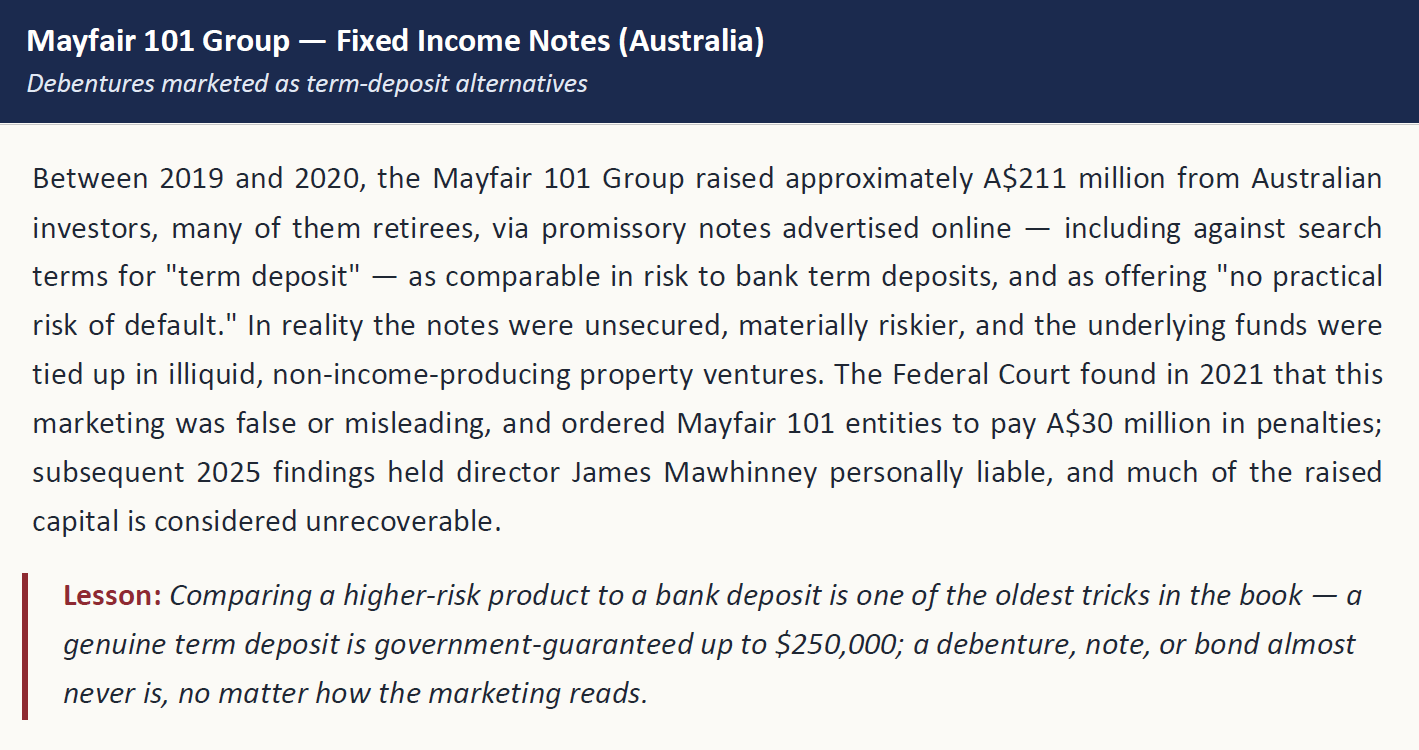

When "Guaranteed" Was a Lie

Three case studies where the promise of certainty was the fraud, not the feature.

The case studies below share a single pattern: returns that were too smooth or too certain relative to what the market was doing. That smoothness was not a sign of skill — it was the fraud.

Red Flags Worth Repeating

The five signals that separate a probability story from a guarantee story.

• Any return advertised as "guaranteed," "risk-free," or "no practical risk of default" outside of a government-guaranteed bank deposit.

• Returns that are unusually smooth or consistent across both rising and falling markets — the Madoff signature.

• A product compared to a term deposit or bond without the same regulatory protections behind it — the Mayfair signature.

• Pressure to invest quickly, difficulty withdrawing funds when requested, or reliance on personal relationships to skip verification.

• An adviser or promoter who cannot be verified on ASIC’s Financial Advisers Register, or who is not the correct holder of the AFS licence they claim.

How to Overcome the Guarantee Instinct

Six practical steps that redirect the emotional pull of certainty toward evidence-based, risk-managed decisions.

The fear of loss and the pull toward guarantees are not weaknesses to overcome by willpower — they are hard-wired responses that even sophisticated investors experience. The task is not to feel differently but to build a decision process that behaves rationally regardless of how the market feels in any given month. The steps below are what an experienced adviser will typically walk a client through, in roughly this order.

1. Separate the emotion from the decision — name what you are actually afraid of

Almost every client who asks for a “guarantee” is really asking about one of three specific fears: running out of income in retirement, losing capital they cannot rebuild, or being blamed for a bad outcome. Each has a different, targeted solution — an income floor from annuities or defensives, a capital-preservation sleeve, or a documented statement of advice. “I need a guarantee” is rarely the actual requirement; it is the emotional shorthand for one of these three.

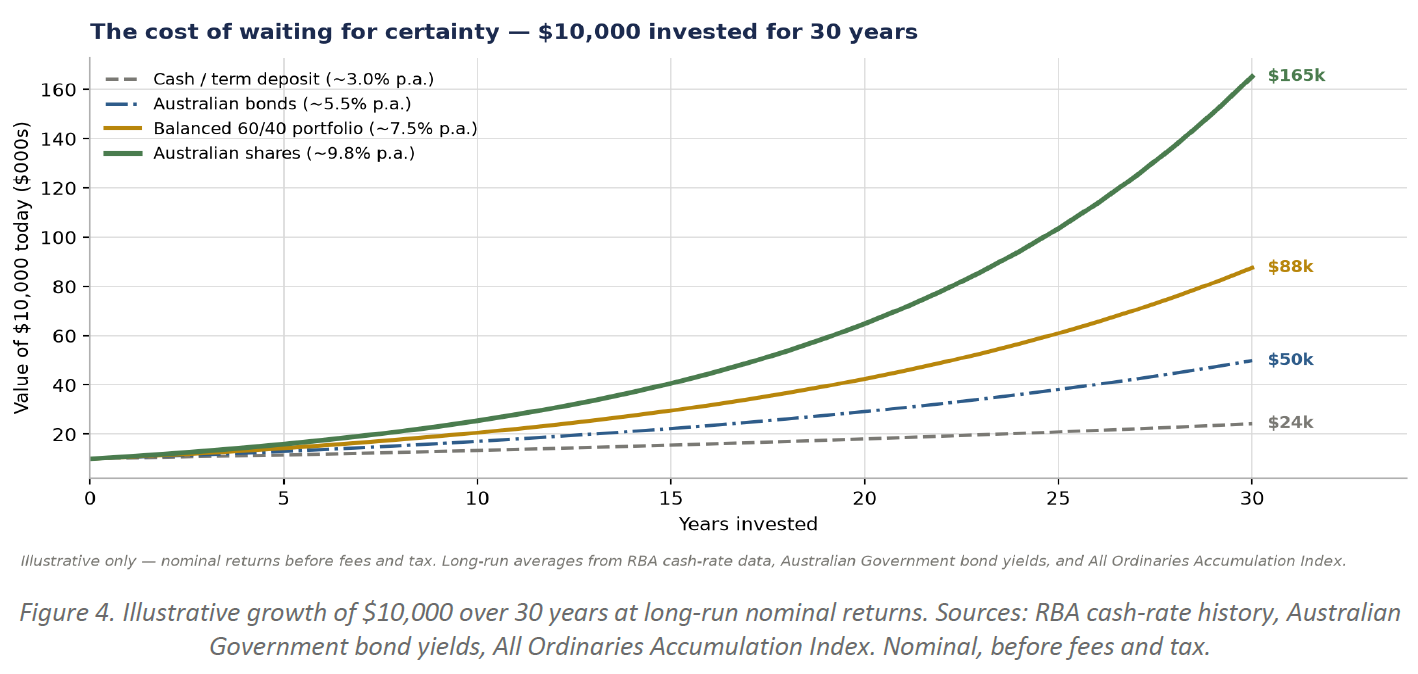

2. Make the cost of avoidance concrete

Loss aversion makes the pain of losing feel roughly twice as sharp as the joy of gaining. Left unmanaged, this bias pushes investors into cash and term deposits — which feel safe but carry their own quiet risk: falling behind inflation, and forgoing decades of compounding. The chart below shows what $10,000 becomes over 30 years across four Australian investment options, using long-run average returns. Sitting in cash is not “no risk” — it is a near-guaranteed erosion of purchasing power.

INVESTOR TAKEAWAY

Think of this as “the cost of certainty.” Cash may feel like the safest choice, but over a 30-year horizon it forgoes roughly $140,000 of wealth per $10,000 invested versus a diversified share portfolio. That gap is what the desire for certainty actually costs you.

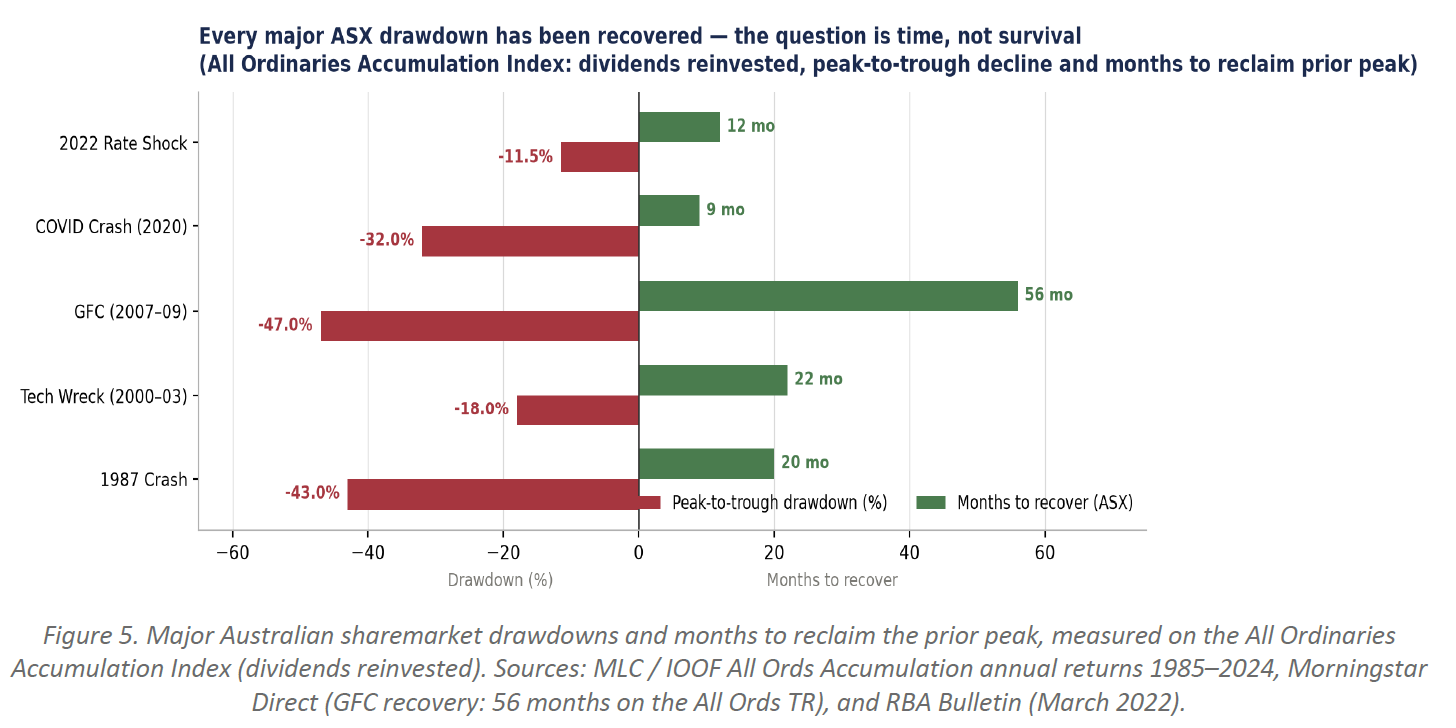

3. Reframe drawdowns as time, not survival

Clients rarely fear market losses in the abstract — they fear a permanent loss. Australian market history says something different: every major drawdown, including the deepest, has been fully recovered. What varies is time. Measured on the All Ordinaries Accumulation Index — which reinvests dividends, and is the honest benchmark for a long-term investor — the GFC took roughly four-and-a-half years to reach a new peak; COVID took nine months; the 1987 crash was recovered inside two years. Because Australian dividends run around 4% per year, reinvested income compresses recovery times materially versus the price-only index that headlines usually quote. The right question is not “will markets fall?” (they will, repeatedly) but “is my time horizon long enough that history says a full recovery is very likely?”

4. Match your time horizon to the asset, not the other way around

The single most useful discipline is aligning money to when you actually need it. Cash and short-dated fixed income for anything you might spend in the next one to three years; growth assets (Australian and global shares, listed property) for money you will not need for at least seven to ten years; private markets and illiquid strategies for money you can genuinely lock away for a decade or more. When time horizon is right, short-term volatility stops being a threat to the plan — it becomes background noise.

5. Automate the decision so emotion cannot override it

Regular contributions, dollar-cost averaging into diversified funds, pre-set rebalancing rules, and written investment policy statements all serve one purpose: removing the moment-by-moment decision to buy or sell. The Vanguard research on the value of advice (“Adviser’s Alpha”) estimates that behavioural coaching alone — keeping clients invested through downturns — adds roughly 1.5% per year to net returns, more than any other single adviser contribution. Systems beat willpower.

6. Verify every counterparty on the licensed registers before signing

The frauds in this issue — Caddick, Mayfair 101, Madoff — were all avoidable at the point of contact. In Australia, two free public checks catch the majority of investment scams: ASIC’s Financial Advisers Register (to confirm the adviser is authorised under the AFS licence they claim) and Moneysmart’s Investor Alert List (which flags entities unlicensed to operate in Australia). A five-minute check before every new investment is the single highest-yield fraud prevention available.

INVESTOR TAKEAWAY

None of these steps eliminate the emotional pull of “guaranteed” — they redirect it toward a plan that behaves rationally when markets do not. That, in practice, is what a genuine near-certainty looks like: a disciplined process, held over a long horizon, and verified at every step.

Bringing It Together

What actually separates a genuine near-certainty from a fraudulent one.

Both public and private markets reward the same underlying instinct — discipline over a defined horizon — but the mechanism differs. In public markets, time alone does most of the work: longer holding periods have historically compressed the range of outcomes toward a near-certain positive result. In private markets, time must be paired with structure: vintage diversification, manager selection, and an understanding that early paper losses are part of the design, not a signal to redeem.

Clients rarely ask for a guarantee because they misunderstand risk. They ask because the emotional weight of a potential loss outweighs, in the moment, their assessment of probability. The most effective response is not to dismiss the desire for certainty but to redirect it: toward diversification, appropriate time horizons, and verified, licensed products that manage risk rather than pretend to eliminate it. Every fraud in this issue targeted intelligent, often financially literate people; the common thread was not a lack of sophistication but a want for certainty strong enough to override healthy scepticism.

"No single year, and no single fund, comes with a guarantee. But a well-constructed portfolio, held over a genuinely long horizon and diversified appropriately, has historically turned favourable odds into something very close to certainty."

• NYU Stern (Aswath Damodaran) — S&P 500 total-return dataset, 1928–2025.

• MLC / Vanguard / Cambridge Associates — Australian All Ordinaries Accumulation Index history, 1900–2023.

• Cambridge Associates — US Private Equity and US Venture Capital Benchmark Statistics (quartile IRR ranges).

• ASIC media releases 21-312MR and 21-364MR — Maliver Pty Ltd (Caddick) and Mayfair 101 Group findings.

• U.S. Department of Justice / SIPC — Madoff Victim Fund distributions and recovery figures (2024).

• Federal Court of Australia — ASIC v Mayfair Wealth Partners judgments, 2021 and 2025.

• Reserve Bank of Australia Bulletin (March 2022) — Australian securities markets through the COVID-19 pandemic.

• Morningstar Direct — S&P/ASX All Ordinaries Total Return Index drawdown and recovery analysis (GFC peak to recovery: 56 months).

• MLC / IOOF Investment Central — All Ordinaries Accumulation Index annual returns, 1985–2024.

• Vanguard Research — Putting a value on your value: quantifying Vanguard Adviser’s Alpha (behavioural coaching estimate).

• ASIC Moneysmart Investor Alert List and Financial Advisers Register (moneysmart.gov.au).

Disclaimer

General information only.This newsletter does not take into account your personal objectives, financialsituation or needs and should not be relied upon as personal financial advice.Case studies are drawn from publicly reported regulatory and court findings andare provided for educational purposes. Historical and illustrative datareferenced includes S&P 500, ASX All Ordinaries Accumulation, and CambridgeAssociates private-markets benchmarks; past performance is not a reliableindicator of future performance, and private-markets figures reflectindustry-wide benchmarks rather than any specific fund. Please speak with youradviser before making any investment decision, and verify any adviser orproduct on ASIC’s registers before investing.