Will AI Lead to Mass Unemployment?

"History has witnessed three great automation waves. Each time, the fears were real, the disruption was painful — and the labor market ultimately adapted. But this time, the adversary can think."

The question hashaunted every major technological shift in modern history. When the mechanicalloom displaced hand weavers in the 1800s, the Luddites smashed machines inprotest. When computers arrived in the 1970s, economists warned of an officeapocalypse. When industrial robots swept into factories in the 1990s, entiremanufacturing towns hollowed out. And now, as artificial intelligence writescode, analyzes documents, draws designs, and holds customer serviceconversations, the oldest fear is back — dressed in a new suit.

But this time,something is categorically different. Previous automation waves were mostlymechanical: they displaced muscle. The Industrial Revolution replaced physicallabor; the IT Revolution replaced clerical, rule-following cognition. AI, forthe first time, displaces judgment. It can draft an email, interpret a legalclause, synthesize a research paper, and recognize patterns across millions ofdata points simultaneously. The white-collar knowledge worker — previously thebeneficiary of automation — is now in the crosshairs.

"The first automation wave to threaten non-routinecognitive tasks — AI doesn't just replace hands, it replaces minds."

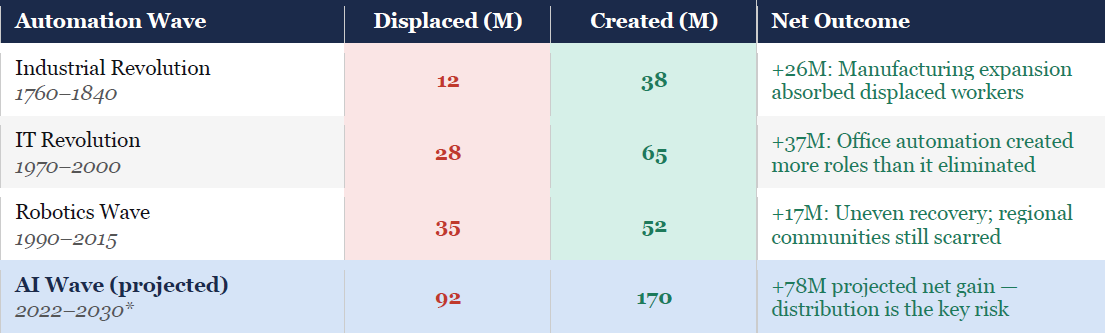

The dataemerging from 2024–2026 is striking, if nuanced. The World Economic Forum's Futureof Jobs Report 2025 — drawing on surveys of over 1,000 employersrepresenting 14 million workers across 55 economies — projects 92 million jobsdisplaced by 2030, with 170 million new roles created, a net positive of 78million. Goldman Sachs, in their landmark 2023 research paper, estimated thatgenerative AI could expose the equivalent of 300 million full-time jobsglobally to automation — though crucially, this refers to exposure totask-level automation, not wholesale elimination. Most jobs exposed to AIwill be augmented, not replaced.

What do thereal-time numbers show? According to Challenger, Gray & Christmas,approximately 55,000 U.S. layoffs in 2025 were directly attributed byemployers to AI — less than 5% of 1.17 million total job cuts that year.Independent modeling using BLS and BEA data estimates broader AI-attributabledisplacement at 200,000–355,000 positions across 2025 when accounting for jobsquietly eliminated rather than formally announced. The headline numbers mask acrucial truth: the transition is not uniform. It is surgical, sector-specific,and generationally lopsided.

AUTOMATION WAVES —HISTORICAL DISPLACEMENT VS. CREATION

The ATM analogy offers instructive historical comfort: when ATMs arrived in the 1970s, economists predicted the end of bank tellers. Instead, lower branch operating costs led banks to open more branches, increasing total teller employment while shifting the role toward relationship management. Whether AI follows the same pattern depends entirely on whether productivity gains are recycled into expansion — or simply extracted as margin. Goldman Sachs notes that over 85% of U.S. employment growth since 1940 has come from technology-driven job creation.

The Jobs at Risk — and the Roles That Remain

Asector-by-sector breakdown of automation vulnerability, and where durableemployment will live.

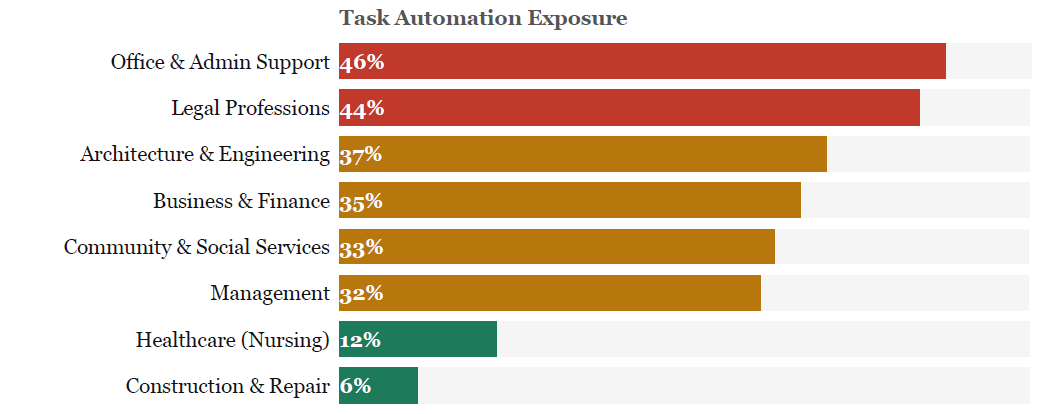

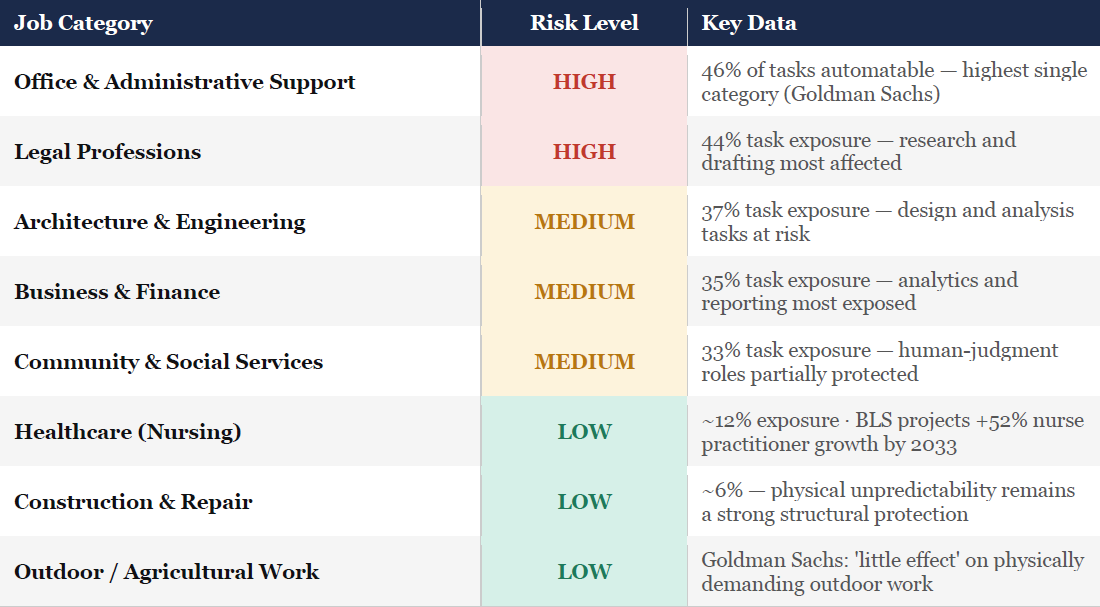

Not all jobsface equal peril. The critical variable is not education level — it is taskcomposition. Goldman Sachs's analysis of over 900 occupations in the O*NETdatabase found that office and administrative support roles face the highestautomation exposure (46% of tasks automatable), followed by legal work (44%),architecture and engineering (37%), and business and financial operations(35%). Roles built around physical variability, emotional attunement, and novelproblem-solving in unpredictable environments are structurally resilient.

TASK AUTOMATION EXPOSURE BY SECTOR (Goldman Sachs / O*NET Analysis)

The IMF's 2024 World Economic Outlook found that roughly 40% of jobs globally face meaningful AI exposure — rising to approximately 60% in high-income, digitized economies. Critically, the IMF distinguishes between exposure (tasks can be automated) and displacement (workers are replaced): in advanced economies, high exposure is roughly split between jobs at risk of being degraded and those likely to be complemented and enhanced by AI tools.

In practical terms, the 2025 layoff data tells a consistent story. Amazon eliminated 14,000 corporate roles, explicitly linking the decision to AI-enabled leaner structures. Salesforce reduced its customer support workforce by 4,000, with its CEO stating AI handles a substantial share of its support workload. Workday cut approximately 1,750 roles — 8.5% of its workforce — to reallocate toward AI investment. Microsoft eliminated roughly 15,000 positions. These are real and significant disruptions concentrated in knowledge-work roles at the entry and mid tiers.

JOB RISK BREAKDOWNBY CATEGORY

PwC's 2025 Global AI Jobs Barometer adds a counterintuitive finding: wages are growing twice as fast in industries most exposed to AI, compared to those withlow AI exposure. Revenue growth in AI-intensive sectors has accelerated sharply since 2022. The signal is clear — the workers who prosper in this transitionare not those who avoid AI, but those who most effectively direct it.

"AI is raising the productivity ceiling for adaptable workers. The acute risk falls on a narrower group: those in high-exposure roles with limited access to retraining. These are the workers that policy must prioritize."

What Our Children Should Learn — and What We Should Build

A forward-looking view of the skills, sectors, and policy architecture that will define durable prosperity for the next generation.

We have a rare advantage that our predecessors in every prior automation wave did not: we can see this coming. The Luddites had no forecast. The factory workers displaced by globalization in the 1990s had no roadmap. We have research institutions, labor economists, and increasingly accurate models of task-level automation risk. The question is whether we will use this foresight or squander it.

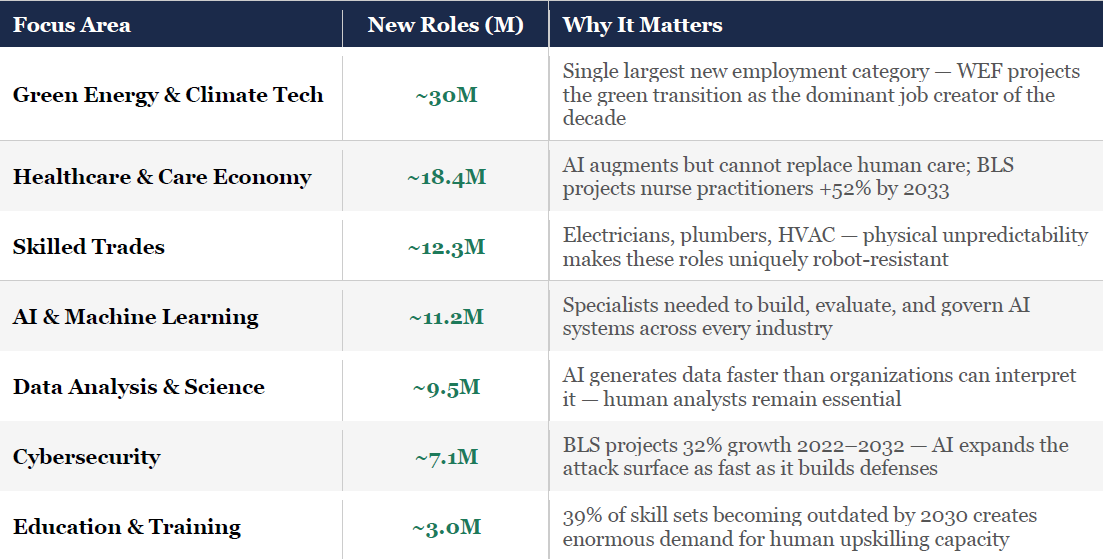

The WEF's Future of Jobs Report 2025 is explicit about what skills will matter most. Technological literacy — AI and big data, networks and cybersecurity — tops the list. But what is notable is the second tier: creative thinking, resilience, analytical thinking, leadership and social influence, and curiosity as a durable habit. Eight of the top ten skills identified are what economists call non-automatable human capabilities. The report projects that 39% of existing skill sets will become outdated by 2030 — down from 57% in 2020, a sign that early upskilling efforts are beginning to narrow the gap.

Singapore's SkillsFuture program remains the most instructive policy model globally: every citizen above 25 has access to a substantial individual learning credit redeemable across thousands of certified courses, tied explicitly to industrial priorities in AI, green economy, and care services. The program demonstrates that proactive, government-anchored retraining at scale is achievable — and that it must be tied to real labor market demand, not generic credential accumulation.

FASTEST-GROWING ROLES 2025–2030 (WEF / BLS Projections)

The historical record on technological transitions offers a conditional optimism. The agricultural labor force fell from over 60% of U.S. employment in the 1800s to less than 2% today — yet total employment did not collapse. Manufacturing followed the same arc. Goldman Sachs notes that roughly 60% of workers today hold jobs in occupations that did not exist in 1940. Every prior wave created unimaginable new categories of work.

But the conditional clause matters enormously. The transition works when: the new jobs arrive in sufficient quantity and geographic proximity; the displaced workers have genuine pathways to retraining; and the productivity gains are distributed broadly enough to sustain consumer demand. None of those conditions are guaranteed in the current transition.

THE FOUR WAVES — A HISTORICAL TIMELINE

Industrial Revolution · 1760–1840

Physical automation displaces agricultural and textile labor

Steam engines, mechanical looms. Fear: mass unemployment. Reality: manufacturing expansion absorbed displaced workers; new jobs were literally unimaginable to the prior generation.

IT Revolution · 1970–2000

Computers eliminate clerical, rule-following cognitive roles

ATMs, spreadsheets, databases. Fear: office apocalypse. Reality: bank teller employment increased as lower costs enabled branch expansion; total office employment grew.

Robotics Wave · 1990–2015

Industrial robots reduce manufacturing employment

Acemoglu & Restrepo's research found each additional robot per 1,000 workers reduced local employment by approximately 0.2 percentage points. Recovery was uneven and geographically concentrated.

AI Wave · 2022–Present

Generative AI targets non-routine cognitive and creative work

First wave to meaningfully threaten judgment-based, white-collar roles. WEF projects net +78M jobs by 2030, but the skills gap, retraining timeline, and geographic concentration of new roles are the decisive variables.

"The question is no longer whether AI will transform the labor market. It already has. The question is whether we design the transition or merely survive it."

The answer to the title question is this: AI will lead to significant, painful, and unequal disruption. But mass unemployment — defined as a sustained, secular collapse of total employment — is not the central-case outcome supported by current evidence. The WEF's net gain of 78 million jobs by 2030 is the institutional consensus anchor.

What is genuinely uncertain is the distribution of those outcomes — whether the gains and losses fall on the same workers, in the same places, within a timeframe that allows adaptation. The 41% of employers planning workforce reductions due to AI are not outliers; they are the leading edge of a structural shift already underway. The obligation, for those of us positioned to shape that shift, is to ensure the productivity gains are reinvested in the human capacity to participate in what comes next.

• World Economic Forum Future of Jobs Report 2025 (Jan 2026, 1,000+ employers, 14M workers, 55 economies)

• Goldman Sachs "The Potentially Large Effects of AI on Economic Growth" — Briggs/Kodnani (2023)

• IMF World Economic Outlook 2024

• Challenger, Gray & Christmas Year-End 2025 Report (confirmed direct AI attribution figure: ~55,000)

• PwC Global AI Jobs Barometer 2025

• U.S. Bureau of Labor Statistics Occupational Projections 2023–2033

• McKinsey Global Institute — The Economic Potential of Generative AI (2023)

• Acemoglu & Restrepo, "Robots and Jobs: Evidence from US Labor Markets" (2020, Journal of Political Economy)

• BEA / independent displacement modeling methodology (daveshap.substack.com, Feb 2026)