2026 Tax, Super & Centrelink — Part III: Centrelink, SMSF Strategy & Investor Actions

The Centrelink Equation: New Rates, New Deeming, and the Part-Pension Sweet Spot

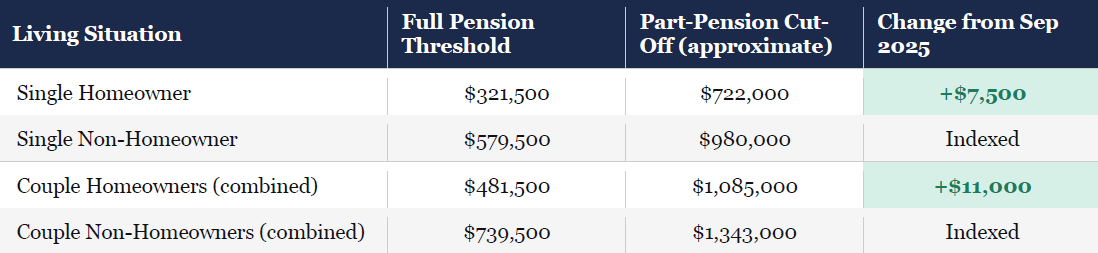

From 20 March 2026, more than 2.6 million Australians receiving the Age Pension saw significant changes to their payment rates, means test thresholds, and — critically — deeming rates. For investors approaching or in retirement, the interaction between these levers and portfolio structure can mean tens of thousands of dollars in annual income.

Age Pension Rate Increase — March 2026

Assets Test — New Cut-Off Limits (from 20 March 2026)

The upper threshold — the maximum assets you can hold and still receive any part-pension — has increased, because the higher base pension rate pushes the taper calculation further before it hits zero.

The family home remains fully exempt from the assets test. Regardless of its value, the principal place of residence does not count toward the assets test. This remains one of the most significant structural features of Australia's retirement income system, and continues to reward home ownership strategies over cash or financial asset accumulation.

Deeming Rates Rise — A Silent Pension Reducer

The most impactful and least-discussed change from 20 March 2026 is the increase in deeming rates. Deeming is the rate of return Centrelink assumes your financial assets earn — regardless of what they actually earn. Both rates increased by 0.5 percentage points:

Worked Example: Patricia holds $420,000 in an account-based pension and owns her home. Under the March 2026 deeming rates, her assumed income is approximately $451/fortnight. Against the singles income test free area ($212/fortnight), Centrelink deems she has $239 excess per fortnight, reducing her pension by $0.50 for each excess dollar — a pension reduction of approximately $119.50/fortnight or roughly $3,107 per year. This is regardless of her actual investment returns. If her portfolio yields less than 3.25%, she is being penalised by the deeming calculation for underperforming the assumed rate.

Rising deeming rates reduce Age Pension entitlements even without a portfolio change. If you are receiving a part-pension and hold significant financial assets in cash or low-yielding term deposits, the March 2026 deeming rate increase has likely already reduced your fortnightly payment. Review your entitlement now — and consider whether repositioning assets into returns that at least match the 3.25% upper deeming rate is appropriate. Centrelink must be notified of asset changes within 14 days.

The Part-Pension Sweet Spot: Counterintuitive Maths

One of the most important planning insights from the 2026 threshold changes is the non-linear relationship between superannuation balance size and total annual income. A single homeowner with $350,000 in super, drawing down and receiving a substantial part-pension, may generate more total annual income than one with $630,000 in super and no pension entitlement — purely because of the pension interaction.

"The question is not just 'how much super do I have?' — it is 'how does my super interact with the Age Pension, and what is my total income across both?'"

This underscores why strategic super drawdown — rather than the minimum required pension payment — can be an effective tool for some retirees. An adviser can model the optimal balance and drawdown rate to maximise total retirement income across super and Centrelink.

The Reform Storm Approaching: What the May 2026 Budget May Bring

No legislation has been passed. But the groundwork is being laid. For the first time in years, Treasurer Jim Chalmers has confirmed that Treasury is actively modelling changes to two of the most significant tax settings in Australian property investment: negative gearing and the 50% capital gains tax (CGT) discount. A Senate Inquiry into the CGT discount tabled its final report in March 2026. The May budget is the earliest any changes would be announced.

"For years, the Albanese government insisted changes to negative gearing and the CGT discount were off the table. Now, with the May 2026 budget approaching, that table appears to be getting very crowded."

Negative Gearing: The Two-Property Cap Proposal

Treasury is modelling a cap of two investment properties per investor for negative gearing deductions. Under this proposal, losses from a third or subsequent investment property would be quarantined — unable to offset salary or other income. They could only be applied against future positive income from that same property or carried forward. No legislation has been introduced, and Labor's formal post-election position remains that changes are 'not something we are proposing.' However, the Prime Minister has declined to rule out reform.

Additionally, a new build carve-out appears to be under consideration — potentially exempting investment in newly constructed properties from any cap, mirroring New Zealand's 2020 reform model. This could significantly favour investors in off-the-plan apartments or house-and-land packages relative to established property investors.

Worked Example: James owns five investment properties, all negatively geared. He currently offsets approximately $65,000 in net rental losses against his $220,000 salary income, generating approximately $24,000 in annual tax savings. Under a two-property cap, the losses from his additional three properties — approximately $42,000 — would be quarantined. His annual after-tax position deteriorates by approximately $16,000. His financial adviser begins modelling a staged portfolio rationalisation, keeping the two properties with the strongest long-term capital growth prospects.

Capital Gains Tax Discount: From 50% to 33%?

The 50% CGT discount — available on assets held for more than 12 months — is the second major reform target. The Senate Inquiry's majority report concluded the discount, combined with negative gearing, has shifted housing ownership away from owner-occupiers and toward investors. A reduction to a 33% discount has been proposed for investment property, with some submissions calling for the discount to be eliminated entirely for multi-property investors.

Reform is not yet law — but strategy review is urgent. The ATO data-matching programme, the Senate Inquiry's conclusions, and the Treasurer's public comments collectively signal this is the highest-probability major tax reform since the Howard government's 1999 CGT changes. Investors with planned property sales in the next 12–24 months should model outcomes under both current and proposed settings, and consider timing implications carefully.

Proponents of reform — including the Grattan Institute and Greens senators — argue the changes would save the budget more than $10 billion over a decade and reduce speculative housing demand, improving affordability for first-home buyers. Opponents, led by the Property Council of Australia, contend that reduced investor incentives will constrict rental supply, pushing rents higher and worsening conditions for the 30% of Australians who rent. The 1985 experience — when negative gearing was briefly quarantined and rents rose in some cities — is frequently cited, though economists dispute whether negative gearing was the primary driver.

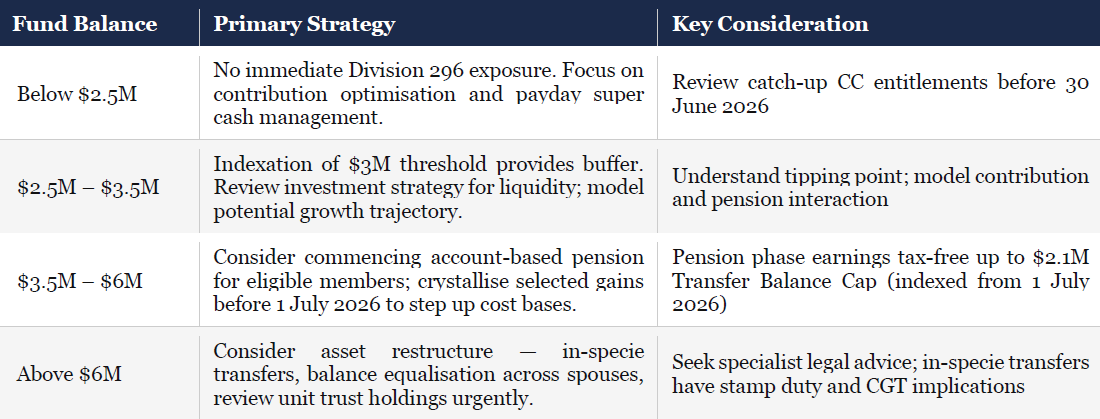

The SMSF Under Pressure: Restructuring for the New Tax Reality

With Division 296 now law and Payday Super arriving on 1 July 2026, the self-managed super fund sector — representing more than 600,000 funds and $900 billion in assets — faces its most complex compliance environment since the introduction of the Transfer Balance Cap in 2017. For SMSF trustees, the combination of higher earnings taxes, tighter ATO scrutiny, and potential future CGT reform demands a clear-eyed assessment of fund structure, asset composition, and liquidity strategy.

The Indirect Asset Tax Trap: Unit Trusts and Companies Inside SMSFs

One of the most technically dangerous aspects of the Division 296 legislation has received remarkably little mainstream attention. SMSFs that hold assets indirectly — through a unit trust or private company — face a significantly more adverse tax outcome than funds holding identical assets directly.

Under the Division 296 rules, SMSFs have a critical opt-in available: they can elect to reset the cost base of all CGT assets to market value at 30 June 2026, so that capital gains accrued before the tax commences are excluded from future Division 296 calculations. This election must be made by the due date for lodging the 2026–27 income tax return. Crucially, the opt-in applies at fund level, not asset-by-asset — all assets are included, even those in unrealised loss positions. This option is available to SMSFs only; retail and industry funds use an approximate factor method for the first four years instead.

However, for SMSFs holding assets indirectly through a unit trust or private company, the cost-base reset provides significantly less protection than it does for direct holdings. While the SMSF can reset the cost base of its units to market value at 30 June 2026, this does not reset the cost base of the underlying assets inside the unit trust or company. When the trust subsequently sells a property or other asset, the capital gain on that underlying asset flows through to the SMSF as income — and that gain is calculated from the asset's original cost base, not the reset value of the units. Pre-existing gains inside the trust remain fully exposed to Division 296. Importantly, this is not an inadvertent gap in the legislation — it is a deliberate policy decision, explicitly documented in the explanatory memorandum to the bill. Investors should not expect a late regulatory fix.

Worked Example — The Unit Trust Problem: An SMSF with a $4 million member balance holds 100% of the units in a unit trust, which in turn owns two commercial properties. The SMSF elects to reset the cost base of its units to 30 June 2026 market value. In 2027–28, the unit trust sells one of the properties, realising a $600,000 capital gain calculated from the property's original purchase price — not from the reset unit value. That gain flows through in full to the SMSF as assessable income and is subject to Division 296. The cost-base reset on the units provides no relief in this scenario. As Sladen Legal principal Phil Broderick has confirmed, the mechanism by which CGT relief applies to directly held assets simply does not extend to gains realised on assets held inside a unit trust or company structure.

ATO SMSF Audit Priorities 2026

The ATO has signalled a major escalation in SMSF compliance activity in 2026. Key areas under scrutiny include:

• Sole purpose test breaches: Any arrangement where SMSF assets — particularly property — provide a benefit to a member, related party, or family member before retirement. The ATO is particularly focused on holiday homes inside SMSFs and on-lending arrangements.

• Non-arm's-length income (NALI): Related-party transactions not conducted on commercial terms can cause the entire income from the asset to be taxed at 45%, not the standard 15%.

• Limited Recourse Borrowing Arrangements (LRBAs): SMSFs must ensure any related-party lending arrangements are at commercial interest rates. The ATO benchmark safe harbour rate for 2025–26 on real property LRBAs is 8.95%.

• Dividend stripping via SMSF: Transferring private company shares to an SMSF to extract franked dividends at super tax rates remains an active ATO target (TA 2015/1 remains in force).

• Incorrect valuations: All SMSF assets must be valued at market value annually. Outdated or internally-generated valuations of property or unlisted investments are a compliance flashpoint.

SMSF Restructuring Strategies: What Advisers Are Recommending

SMSF property in 2026: still permitted, but rules are strict. SMSFs can continue to purchase residential and commercial property in 2026. Residential property cannot be purchased from related parties and cannot be used by members or their families. Commercial property can be purchased from a related party at market value and leased back on arm's-length terms. Minimum recommended fund balance for SMSF property investment is $200,000–$300,000. A corporate trustee structure is strongly preferred for asset protection and estate planning flexibility.

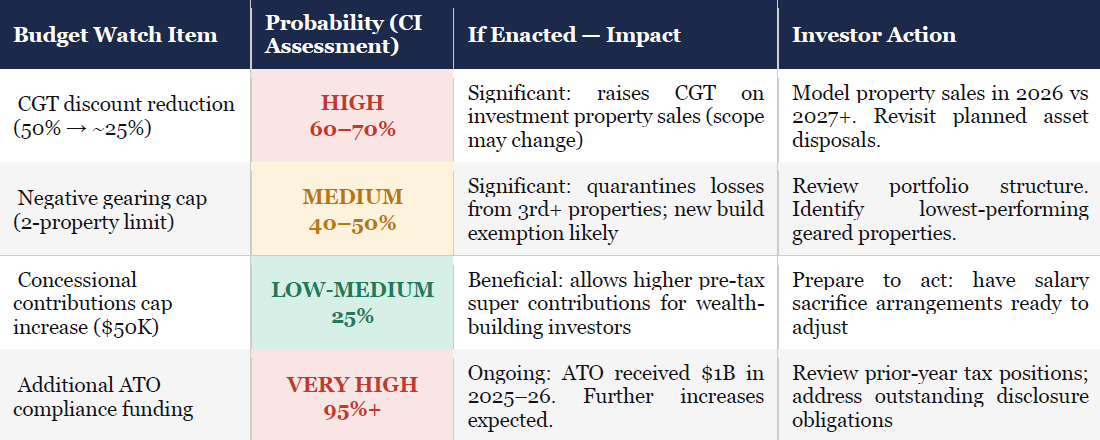

The May 12 Budget: What Investors Should Watch and Do Now

Treasurer Jim Chalmers will hand down the 2026–27 Federal Budget on 12 May 2026 — the Albanese government's first budget after its stronger-than-expected 2025 election victory and fifth budget overall. This is the budget that will determine whether the CGT discount reform and negative gearing cap move from speculation to statute. For investors, this is potentially the most consequential May night since the introduction of the superannuation guarantee in 1992.

What CBA and Westpac Are Forecasting

Commonwealth Bank's economics team has moved furthest on the record: its economists explicitly forecast that the CGT discount will be reduced from 50% to approximately 25%, implemented at the time of the May Budget. They note this will weigh on property prices in 2026's second half, estimating total dwelling price growth for the calendar year at slightly above 5% — a material deceleration from 2025.

Westpac broadly concurs on the direction but is more cautious on timing, noting that political capital and Senate negotiation complexity may push implementation to the 2026–27 income year or later. Notably, BDO's pre-budget submission explicitly calls for the concessional contributions cap to be raised to $50,000 — nearly double the current $30,000 limit. While this is an industry wish rather than a government commitment, the post-election political environment gives Labor more room to make the system appear both fair (through Division 296) and generous (through a higher CC cap) simultaneously.

Budget Watch — CI Probability Assessment

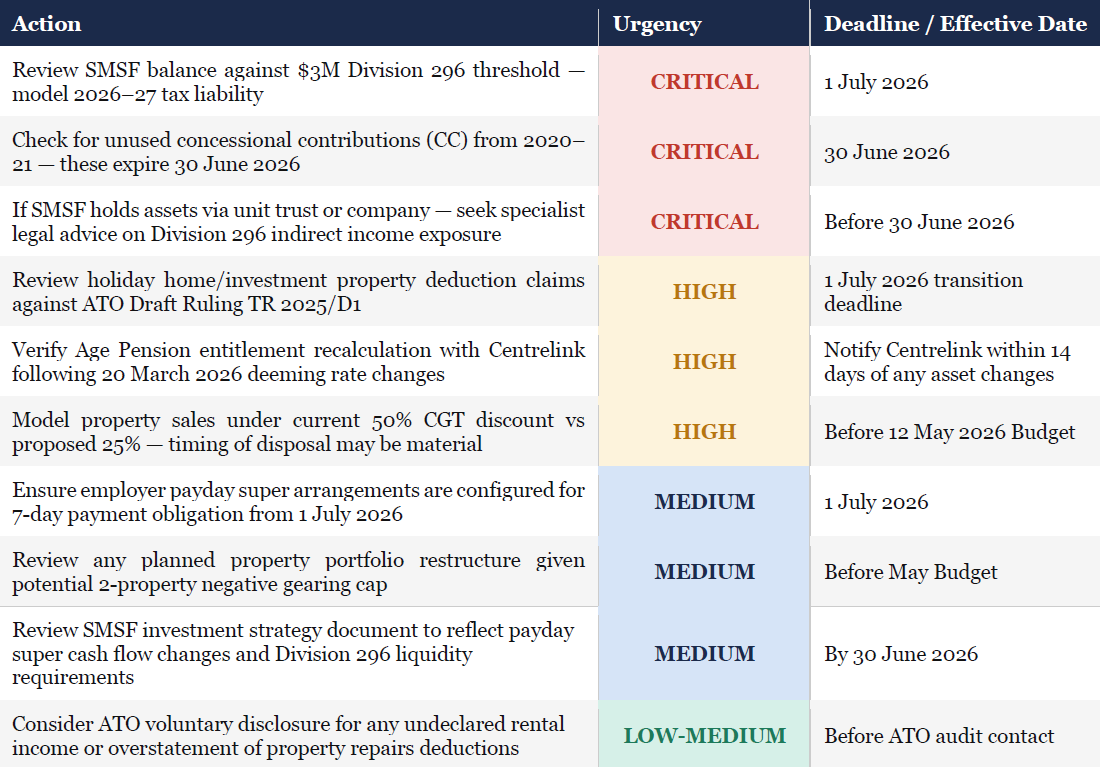

The Definitive 2026 Investor Action Checklist

"The intersection of Division 296, Payday Super, the March 2026 Centrelink changes, and the looming May Budget creates a period of reform density that Australia's investment community has not experienced in a generation. Investors who act now hold the initiative. Those who wait for certainty may find the landscape has shifted beneath them."

A Note on the Opportunity Within the Reform

It is worth concluding with a counterintuitive observation. The reform environment of 2026, while genuinely complex and in some respects financially demanding, also creates meaningful planning opportunities for investors who engage proactively. The Division 296 threshold is indexed — which means those who restructure now to manage their balance relative to the threshold are not locked in permanently. The potential CGT discount reduction, if combined with a new-build carve-out for negative gearing, could create a structural advantage for investors in the construction sector.

The deeming rate changes, while reducing some pension entitlements, also create a clear incentive to seek investment returns that at least match the 3.25% upper deeming rate — which is, frankly, not a high bar in a 2026 interest rate environment. Australia's tax and retirement systems are dynamic, not static. The investors who understand the rules well enough to plan around them — and who work with advisers who are across the detail — will, as in prior reform cycles, emerge in stronger positions than those who simply absorb the changes passively. That has always been the central premise of The Long View.

Further Issues Every Informed Investor Should Know

The following topics are not central to the newsletter's primary scope, but are flagged here for completeness — each has real relevance for specific investor situations.

Division 296: The Cost-Base Reset Election — Details Matter

As noted earlier in the article, SMSFs can elect to reset CGT asset cost bases to market value at 30 June 2026 — a one-time opt-in that removes pre-2026 unrealised gains from all future Division 296 calculations. The key details investors and trustees must understand:

• Fund-level election only: The choice applies to all CGT assets in the fund at 30 June 2026 — you cannot cherry-pick individual assets. This means assets in an unrealised loss position will also have their cost base reset upward, eliminating future capital loss offsets on those assets.

• First-year rule: For the 2026–27 income year only, Division 296 liability is determined by reference to the member's closing balance at 30 June 2027 — not the opening balance. Members who reduce their Total Super Balance below $3M by 30 June 2027 will not be liable for Division 296 in that first year. This is a meaningful short-term planning opportunity for members sitting close to the threshold.

• Deadline: The election must be lodged by the due date for the fund's 2026–27 income tax return — typically 15 May 2028 for funds with a tax agent.

• Industry and retail funds: These use an ATO-approved factor method for the first four income years (2026–27 through 2029–30) to calculate historical earnings rather than a cost-base reset.

• Death benefits interaction: Where an SMSF member dies and their super balance passes to a non-dependent, Division 296 assessments interact with the estate in specific ways depending on the year of death. In the first year of the regime (2026–27), a member who dies on or before 30 June 2027 will not be subject to any Division 296 assessment at all. From 2027–28 onwards, assessments in the year of death are calculated on a pro-rata basis to the date of death. Trustees should review member death benefit nominations to ensure they interact properly with the new tax regime

SMSF Death Benefits and Estate Planning Under Division 296

Division 296 introduces a new dimension to SMSF estate planning. For members with balances above $3 million, the size and composition of the fund's assessable earnings at the date of death affect the final Division 296 liability — though notably, no Division 296 assessment arises at all if death occurs on or before 30 June 2027. From 2027–28 onwards, estate planning strategies that were optimal before Division 296 — including the timing of pension commutations and benefit payments — should be reviewed by a specialist SMSF lawyer and financial adviser.

Binding Death Benefit Nominations and Division 296: A binding nomination that directs super to a tax-dependent (spouse or financially dependent child) on death generally produces a better after-tax outcome than directing benefits to a non-dependent estate beneficiary — the latter triggers a 17% or 32% death benefits tax on the taxable component. Division 296 adds further reason to ensure nominations are current, binding rather than non-binding, and reviewed in light of each member's super balance trajectory.

Medicare Levy Surcharge Thresholds

The Medicare Levy Surcharge (MLS) — an additional 1–1.5% tax on higher-income earners who do not hold appropriate private hospital insurance — applies for 2025–26 at the following thresholds. The 2026–27 thresholds have not yet been published by the ATO.

* The family threshold increases by $1,500 for each MLS dependent child after the first.

For a single individual earning $150,000 without qualifying private hospital cover, the MLS rate of 1.25% applies — an additional tax cost of $1,875 per year. Holding an appropriate private hospital cover policy will typically cost less than this amount, making cover financially worthwhile at this income level regardless of health considerations.

Crypto and Alternative Assets in SMSFs: Valuation Rules Tighten

Cryptocurrency and digital assets held inside SMSFs must be valued at market value at 30 June each year for reporting purposes. With Division 296 now applying realised-earnings taxation, crypto assets inside high-balance SMSFs will generate a Division 296 assessment in any year where they are sold at a gain. The ATO's data-matching capability now extends to crypto exchanges via third-party reporting, and undisclosed crypto gains inside SMSFs are a 2026 audit priority. SMSFs must also have a documented investment strategy that specifically addresses crypto as an asset class — generic strategies that predate the fund's crypto holdings are non-compliant.

Aged Care and the Assets Test: An Emerging Interaction

For investors moving into residential aged care, the assets test interaction between aged care means testing and the Age Pension assets test creates a complex dual-assessment environment. The refundable accommodation deposit (RAD) paid on entry to aged care is exempt from the Age Pension assets test but is included in the aged care means test. For families with large super balances, early planning — ideally three to five years before likely aged care entry — can materially reduce lifetime aged care costs. Division 296 adds further complexity for those with TSBs above $3 million, as the interaction between super pension drawdowns and aged care means testing requires modelling by a specialist aged care financial adviser.

• ATO — Better Targeted Superannuation Concessions (Division 296) guidance, January 2026

• SBS News — Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026 passage, March 2026

• Services Australia — Age Pension income and assets test thresholds, 20 March 2026

• Wealth Copilot — Age Pension Changes March 2026 analysis

• Hudson Financial Planning — The Super Sweet Spot (March 2026) and ATO Holiday Home Negative Gearing ruling

• Paris Financial — 2026 Super and Tax Changes overview

• HLB Mann Judd — Division 296 SMSF Changes, December 2025

• Finance Directory — Negative Gearing and CGT Changes 2026

• Property Investment Professionals — Negative Gearing Cap & CGT Changes 2026 Investor Guide

• The Senior / SBS News — 2026 Money Changes summary, January 2026

• Property Council of Australia — submission opposing CGT and negative gearing reform

• Senate Inquiry into CGT Discount — Final Report, March 2026

• DuoTax — Superannuation Tax Changes 2026 overview

• SMS Magazine — Sladen Legal / Phil Broderick analysis: Division 296 and indirect asset income, February 2026

• TAMIM Asset Management — Super Tax Reforms and SMSF Trustee implications, October 2025

• Boa & Co. Chartered Accountants — Super Tax Overhaul 2026: The $3M Rule for SMSF Trustees

• SMSF Wiz — Complete Guide to SMSF Property Investment 2026

• Citadel Agency — SMSF Property Rules 2026: What You're Allowed to Buy

• BDO Australia — 2026–27 Federal Budget preview and pre-budget submission

• CBA Economics — Housing Forecasts 2026 (CGT discount and property price modelling)

• Westpac Economics — Big Banks Diverge on Housing Forecasts, March 2026

• Grant Thornton Australia — Division 296: Key Elements of the New Legislation, March 2026

• ATO — Medicare Levy Surcharge income thresholds and rates 2025–26

• ATO — Crypto assets and tax: SMSF reporting obligations 2026

• ASIC MoneySmart — Death benefit nominations and super estate planning

• MLC / Superguide — Division 296 cost-base reset election: what trustees need to know

• Australian Aged Care Quality and Safety Commission — Aged care means testing overview

• Buyers Agency Australia — Negative Gearing 2026 analysis