2026 Tax, Super & Centrelink — Part II: Tax Changes & Property Implications

Tax Relief and New Complexity: The 2026 ATO Landscape

The 2025–26 and 2026–27 tax years bring welcome relief for most Australian taxpayers in the form of personal income tax cuts — but simultaneously introduce new compliance complexity for investors with property portfolios, holiday homes, and SMSF structures.

Stage 3 Tax Cuts — Phase 2 from 1 July 2026

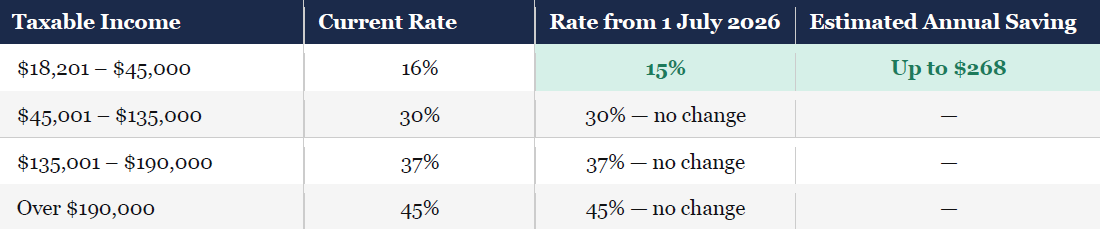

From 1 July 2026, the personal income tax rate applying to taxable income between $18,201 and $45,000 will reduce from 16% to 15% — delivering most taxpayers up to $268 more per year. A further 1% reduction follows in 2027, eventually saving eligible taxpayers up to $536 annually.

Investor note on super contributions: For earners below $45,000, the reduced personal tax rate means concessional super contributions are slightly less advantageous on a pure tax-differential basis (15% contribution tax vs 15% marginal rate). Advisers may recommend shifting to after-tax (non-concessional) contributions to capture the government co-contribution instead.

Holiday Home Negative Gearing: ATO Draft Ruling TR 2025/D1

One of the most consequential changes for property investors with mixed-use holiday homes is ATO Draft Ruling TR 2025/D1, which significantly restricts negative gearing deductions for properties not primarily held for income production. Under the ruling, if a holiday home is used personally for material periods and is not genuinely and primarily available for rental income, the ATO can disallow the deduction of rental losses against other income. Transitional relief applies for existing arrangements until 1 July 2026, after which full compliance is required.

Worked Example: David and Karen own a beachside property at Noosa which they use for four weeks of personal holidays annually and rent through an agent for the remainder. Under current rules, they claim a net rental loss of $22,000 against David's $180,000 salary. Under TR 2025/D1, if the ATO determines the property is not mainly held for income production — applying a qualitative assessment, not just a day-count — those deductions may be disallowed from the 2026–27 income year. Their adviser recommends documenting the property's commercial availability during peak periods and maintaining records of attempted lettings during personally-used weeks.

ATO Data-Matching Intensification: The ATO is actively cross-referencing property income declarations with bank records, state land tax data, and short-stay platform data (Airbnb, Stayz). Undeclared rental income and overclaimed deductions on investment and holiday properties are a 2026 audit priority.

Capital Improvements vs. Repairs: An Ongoing ATO Flashpoint

A persistent area of investor non-compliance — flagged again in 2025–26 — is the misclassification of capital improvements as immediately deductible repairs. The ATO distinguishes clearly: genuine repairs (restoring an asset to its original condition) are immediately deductible; improvements that extend the life or functionality of an asset must be depreciated over time. The ATO has signalled increased data-matching and audit activity in this area.

• ATO — Better Targeted Superannuation Concessions (Division 296) guidance, January 2026

• SBS News — Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026 passage, March 2026

• Services Australia — Age Pension income and assets test thresholds, 20 March 2026

• Wealth Copilot — Age Pension Changes March 2026 analysis

• Hudson Financial Planning — The Super Sweet Spot (March 2026) and ATO Holiday Home Negative Gearing ruling

• Paris Financial — 2026 Super and Tax Changes overview

• HLB Mann Judd — Division 296 SMSF Changes, December 2025

• Finance Directory — Negative Gearing and CGT Changes 2026

• Property Investment Professionals — Negative Gearing Cap & CGT Changes 2026 Investor Guide

• The Senior / SBS News — 2026 Money Changes summary, January 2026

• Property Council of Australia — submission opposing CGT and negative gearing reform

• Senate Inquiry into CGT Discount — Final Report, March 2026

• DuoTax — Superannuation Tax Changes 2026 overview

• SMS Magazine — Sladen Legal / Phil Broderick analysis: Division 296 and indirect asset income, February 2026

• TAMIM Asset Management — Super Tax Reforms and SMSF Trustee implications, October 2025

• Boa & Co. Chartered Accountants — Super Tax Overhaul 2026: The $3M Rule for SMSF Trustees

• SMSF Wiz — Complete Guide to SMSF Property Investment 2026

• Citadel Agency — SMSF Property Rules 2026: What You're Allowed to Buy

• BDO Australia — 2026–27 Federal Budget preview and pre-budget submission

• CBA Economics — Housing Forecasts 2026 (CGT discount and property price modelling)

• Westpac Economics — Big Banks Diverge on Housing Forecasts, March 2026

• Grant Thornton Australia — Division 296: Key Elements of the New Legislation, March 2026

• ATO — Medicare Levy Surcharge income thresholds and rates 2025–26

• ATO — Crypto assets and tax: SMSF reporting obligations 2026

• ASIC MoneySmart — Death benefit nominations and super estate planning

• MLC / Superguide — Division 296 cost-base reset election: what trustees need to know

• Australian Aged Care Quality and Safety Commission — Aged care means testing overview

• Buyers Agency Australia — Negative Gearing 2026 analysis